Archives of “January 3, 2019” day

rssMoney Can't Buy You Love, but What about Happiness?

This Great Graphic is from theEconomist. It is based on the work of two economists, Betsey Stevenson and Justin Wolfers. A recent research paper looks at the relationship between self assessments of one’s well being and the self-reported annual income.

This Great Graphic is from theEconomist. It is based on the work of two economists, Betsey Stevenson and Justin Wolfers. A recent research paper looks at the relationship between self assessments of one’s well being and the self-reported annual income. For nearly 40 years now the conventional wisdom is that money can’t buy happiness. Stevenson and Wolfers challenges that view. Their work finds that consistently in the various countries they look at people were happier (claimed to have higher levels of “life satisfaction”) as drew higher incomes. Moreover, there does not seem to be a point of diminishing returns: the more income the greater the “life satisfaction” ratings. (more…)

$15 Trillion

Someone’s illustrated all the various types and layers of debt we enjoy here in the United States of Indentured Servitude. That pile below next to the Statue of Liberty is what $15 trillion dollars would look like all stacked up:

Five Timeless Rules of Investing Learned From Jesse Livermore

. “My greatest discovery was that a man must study general conditions, to size them up so as to be able to anticipate probabilities.” What did Livermore mean by “general conditions”? He meant the macroeconomic environment and geopolitics. Are they favorable or not favorable to buying stocks? Today, the Fed is raising rates and squeezing the money supply (the monetary base declined last month for the first time in years; a year ago, it was going up 10%.) The war in the Middle East is heating up. These general conditions are not conducive to a bull market, except for gold!

“My greatest discovery was that a man must study general conditions, to size them up so as to be able to anticipate probabilities.” What did Livermore mean by “general conditions”? He meant the macroeconomic environment and geopolitics. Are they favorable or not favorable to buying stocks? Today, the Fed is raising rates and squeezing the money supply (the monetary base declined last month for the first time in years; a year ago, it was going up 10%.) The war in the Middle East is heating up. These general conditions are not conducive to a bull market, except for gold!

2. Learn from wise old men who have experience in the markets. In Reminiscences of a Stock Operator , the author talks about “the Old Turkey,” a “very wise old codger” who counseled Jesse Livermore on making good investment decisions and avoiding mistakes. How can you do this? The best way is to read histories of the great investors such as Warren Buffett, Peter Lynch, John Templeton and J. Paul Getty.

3. Learn your strengths and weaknesses. “We’ve all got a weak spot. What’s yours?” asks the Old Turkey. A good question that we must all answer. “Study mistakes,” he counsels. You don’t learn from your successes, only from your mistakes!

4. Always save some of your gains. “I was again living pretty well, but always saving something, to increase the stake that I was to take back to Wall Street.” Unfortunately, Livermore made the mistake of not living up to his own advice. He leveraged himself too much, and often went bankrupt. By taking some of your gains and investing the funds in alternative investments, such as real estate, art and collectibles, or gold coins, you protect yourself in case you are wrong.

This reminds me of something that happened to me many years ago. I had made a $2 million profit on a penny stock and my wife sat me down and insisted I pay off the mortgage, which was sizeable. I told her I preferred to reinvest the profits in more penny stocks, but she insisted, and I finally agreed with her and paid off the mortgage. It was the best decision “I” ever made! Had I invested the profits in more penny stocks, I would have lost my shirt, because the penny stocks went into a major bear market soon after.

5. Beware the charismatic financial guru! “It cost me millions to learn that another dangerous enemy to a trader is his susceptibility to the urgings of a magnetic personality when plausibly expressed by a brilliant mind.” Oh, how true. I well remember the times I invested in several tax shelters that eventually went bust, because I was thoroughly convinced by a smooth talking salesman who seemed brilliant at the time.

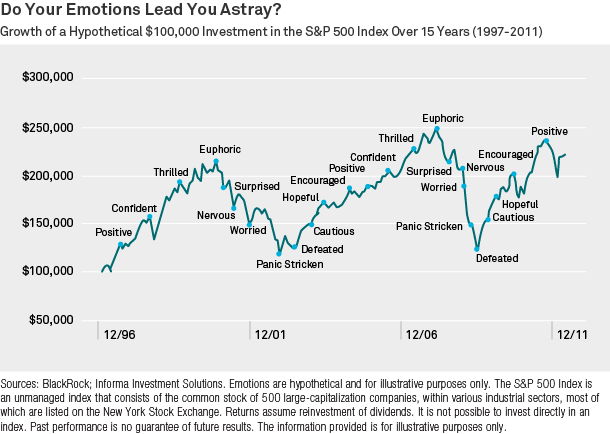

The Emotional Investing Roller Coaster

I love this chart

Thought For A Day

Trading Difficulties -One Liners

Trading Difficulties

- Cut winning trades short even though you know your trade setup is solid.

- Failed to pull the trigger on a perfectly good trade because of fear of loss.

- Let losing trades run hoping for a return to breakeven.

- Added to a losing position in the hope that the market would turn around.

- Made profi ts in the morning but gave them back in the afternoon.

- Became more aggressive after losing money.

- Took unplanned trades when the market suddenly moved.

- Stopped trading or reduced position size after a loss.

- Traded greater position size than prudent money management practice would advise.

- Held trades longer than they should have been held looking for a “home run.”

- Failed to take a perfectly sound setup because the last two trades were losers.

- After a day of big profits, your confidence soared and your trading suffered.

- Consistently made small money but have been unable to elevate your trading performance.

These trading difficulties hurt. They not only hurt your account, but they also cause mental and emotional suffering. No other profession tests your psychology as does trading. These difficulties and unskilled trading behaviors arise from the underlying mental and emotional challenges traders face.

Quotes from Reminiscences of a Stock Operator

From my trove of interesting market quotes, here are my favourite snippets from “Reminiscences of a Stock Operator” by Edwin Lefevre. I enjoyed Reminiscences greatly, both on the first and second readings.While I disagree with some of his pearls of wisdom, many are definitely worth taking on board. For your contemplation:

From my trove of interesting market quotes, here are my favourite snippets from “Reminiscences of a Stock Operator” by Edwin Lefevre. I enjoyed Reminiscences greatly, both on the first and second readings.While I disagree with some of his pearls of wisdom, many are definitely worth taking on board. For your contemplation:

I did precisely the wrong thing. The cotton showed me a loss and I kept it. The wheat showed me a profit and I sold it out. Of all the speculative blunders there are few greater than trying to average a losing game. Always sell what shows you a loss and keep what shows you a profit.If all I have is ten dollars and I risk it, I am much braver than when I risk a million if I have another million salted away.

I’ve got friends, of course, but my business has always been the same – a one-man affair. That is why I have always played a lone hand.

What beat me was not having brains enough to stick to my own game – that is, to play the market only when I was satisfied that precedents favoured my play. There is the plain fool, who does the wrong thing at all times everywhere, but there is also the Wall Street fool, who thinks he must trade all the time. No man can have adequate reasons for buying or selling stocks daily – or sufficient knowledge to make his play an intelligent play.

It happened just as I figured. The traders hammered the stocks in which they figured would uncover the most stops, and sure enough, prices slid off.

For one thing, the automatic closing out of your trade when the margin reached the exhaustion point was the best kind of stop-loss order.

The game taught me the game. And it didn’t spare me rod while teaching.

If somebody had told me my method would not work I nevertheless would have tried it out to make sure for myself, for when I am wrong only one thing convinces me of it, and that is, to lose money. And I am only right when I make money. That is speculating.

I knew of course, there must be a limit to the advances and an end to the crazy buying of A.O.T.-Any Old Thing-and I got bearish. But every time I sold I lost money, and if it hadn’t been that I ran darn quick I would have lost a lot more.

Early that fall I not only was cleaned out again but I was so sick of the game I could no longer beat that I decided to leave New York and try something else some other place. I had been trading since my fourteenth year. I had made my first thousand dollars when I was a kid at fifteen, and my first ten thousand before I was twenty one. I had made and lost a ten thousand stake more than once. In New York I had made thousands and lost them. I got up to fifty thousand and two days later that went. I had no other business and knew no other game. After several years I was back where I began. No-worse, for I had acquired habits and a style of living that required money; though that part didn’t bother me as much as being wrong so consistently.

There were times when my plans went wrong and my stocks did not run true to form, but did the opposite of what they should have done if they had kept up their regard for precedent. But they did not hit me very hard – they couldn’t, with my shoestring margins. My relations with my brokers were friendly enough. Their accounts and records did not always agree with mine, and the differences uniformly happened to be against me. Curious coincidence-not! But I fought for my own and usually won in the end. They always had the hope of getting from me what I had taken from them. They regarded my winnings as temporary loans, I think.

Don’t misunderstand me. I never allowed pleasure to interfere with business. When I lost it was always because I was wrong and not because I was suffering from dissipation or excesses. There were never any shattered nerves or rum-shaken limbs to spoil my game. I couldn’t afford anything that kept me from feeling physically and mentally fit. Even now I am usually in bed by ten. As a young man I never kept late hours, because I could not do business properly on insufficient sleep.

For instance, I had been bullish from the very start of a bull market, and I had backed my opinion by buying stocks. An advance followed, as I had clearly foreseen. So far, all very well. But what else did I do? Why, I listened to the elder statesmen and curbed my youthful impetuousness. I made up my mind to be wise carefully, conservatively. Everybody knew that the way to do that was to take profits and buy back your stocks on reactions. And that is precisely what I did, or rather what I tried to do; for I often took profits and waited for a reaction that never came. And I saw my stock go kitting up ten points more and I sitting there with my four-point profit safe in my conservative pocket. They say you never go broke taking profits. No, you don’t. But neither do you grow rich taking a four-point profit in a bull market.

I think it was a long step forward in my trading education when I realised at last that when old Mr Partridge kept on telling other customers, “Well, you know this is a bull market!” he really meant to tell them that the big money was not in the individual fluctuations but in the main movements-that is, not in reading the tape but in sizing up the entire market and its trend.

The market does not beat them. They beat themselves, because though they have brains they cannot sit tight. Old Turkey was dead right in doing and saying what he did. He had not only the courage of his convictions but also the intelligence and patience to sit tight.

Disregarding the big swing and trying to jump in and out was fatal to me. Nobody can catch all the fluctuations. In a bull market the game is to buy and hold until you believe the bull market is near its end.

Remember that stocks are never too high for you to begin buying or too low to begin selling.

Suppose he buys his first hundred, and that promptly shows him a loss. Why should he go to work and get more stock? He ought to see at once that he is in the wrong; at least temporarily.

The Union Pacific incident in Saratoga in the summer of 1906 made me more independent than ever of tips and talk – that is, of the opinions, surmises and suspicions of other people, however friendly or however able they might be personally. Events, not vanity, proved for me that I could read the tape more accurately than most of the people about me. I also was better equipped than the average customer of Harding Brothers in that I was utterly free from speculative prejudices. The bear side doesn’t appeal any more than the bull side, or vice versa. My one steadfast prejudice is against being wrong.

When I am long of stocks it is because my reading of conditions has made me bullish. But you find many people, reputed to be intelligent, who are bullish because they have stocks. I do not allow my possessions – or my prepossessions either – to do any thinking for me. That is why I repeat that I never argue with the tape.

Obviously the thing to do was to be bullish in a bull market and bearish in a bear market.

… I came to learn that even when one is properly bearish at the very beginning of a bear market it is not well to begin selling in bulk until there is no danger of the engine back-firing.

Of course, if a man is both wise and lucky, he will not make the same mistake twice. But he will make any one of ten thousand brothers or cousins of the original. The Mistake family is so large that there is always one of them around when you want to see what you can do in the fool-play line.

Losing money is the least of my troubles. A loss never troubles me after I take it. I forget it overnight. But being wrong – not taking the loss – that is what does the damage to the pocket book and to the soul.

“I can’t sleep” answered the nervous one.

“Why not?” asked the friend.

“I am carrying so much cotton that I can’t sleep thinking about. It is wearing me out. What can I do?”

“Sell down to the sleeping point”, answered the friend.

He will risk half his fortune in the stock market with less reflection that he devotes to the selection of a medium-priced automobile.

It sounds very easy to say that all you have to do is to watch the tape, establish your resistance points and be ready to trade along the line of least resistance as soon as you have determined it. But in actual practice a man has to guard against many things, and most of all against himself – that is, against human nature.

A speculator must concern himself with making money out of the market and not with insisting that the tape must agree with him. Never argue with it or ask for reasons or explanations.

He should accumulate his line on the way up. Let him buy one-fifth of his full line. If that does not show him a profit he must not increase his holdings because he has obviously begun wrong; he is wrong temporarily and there is no profit in being wrong at any time.

Fear keeps you from making as much money as you ought to.

That was the only one case. There isn’t a man on Wall Street who has not lost money trying to make the market pay for an automobile or a bracelet or a motor boat or a painting.

More than once in the past I had run up a shoe-string in to hundreds of thousands. Sooner or later the market would offer me an opportunity.

The game does not change and neither does human nature.

After I paid off my debts in full I put a pretty fair amount in to annuities. I made up my mind I wasn’t going to be strapped and uncomfortable and minus a stake ever again.

Among the hazards of speculation the happening of the unexpected – I might even say of the unexpectable – ranks high.

I started my buying operations in the winter of 1917. I took quite a lot of coffee. The market however, did nothing to speak of. It continued inactive and as for the price, it did not go up as I had expected. The outcome of it all was that I simply carried my line to no purpose for nine long months.

I trade on my own information and follow my own methods.

He was utterly fearless but never reckless. He could, and did, turn on a twinkling if he found he was wrong.

At the same time I realise that the best of all tipsters, the most persuasive of all salesmen, is the tape.

The speculator’s deadly enemies are: Ignorance, greed, fear and hope. All the statue books in the world and all the rule books on all the Exchanges of the earth cannot eliminate these from the human animal.

On Pat Hearne – He made money in stocks, and that made people ask him for advice. He would never give any. If they asked him point-blank for his opinion about the wisdom of their commitments he used a favourite race-track maxim of his: “You can’t tell till you bet.” He traded in our office. He would buy one hundred shares of some active stock and when, or if, it went up 1 percent, he would buy another hundred. On another points advance, another hundred shares; and so on. He used to say that he wasn’t playing the game to make money for others and therefore would put in a stop-loss order one point below the price of his last purchase. When the price kept going up he simply moved up his stop with it. On a 1 percent reaction he was stopped out. He declared he did not see any sense in losing more than one point, whether it came out of his original margin or out of his paper profits.

“You know, a professional gambler is not looking for long shots, but for sure money. Of course, long shots are fine when they come in. In the stock market Pat wasn’t after tips or playing to catch twenty-points-a-week advances, but sure money in sufficient quantity to provide him with a good sense of living. Of all the thousands of outsiders I have run across in Wall Street, Pat Hearne was the only one who saw in stock speculation merely a game of chance like faro or roulette, but nevertheless had the sense to stick to a relatively sound betting method.

“After Pat Hearne’s death one of our customers who had always traded with Pat and used his system made over a hundred thousand dollars in Luckawana. Then he switched over to some other stock and because he had made a big stake he thought he need not stick to Pat’s way. When a reaction came, instead of cutting his losses he let them run – as though they were profits. Of course every cent went. When he finally quit he owed us several thousand dollars.

And he was right. I sometimes think that speculation must be an unnatural sort of business, because I find that the average speculator has arrayed against his own nature. The weaknesses that all men are prone to are fatal to success in speculation – usually those very weaknesses that make him likable to his fellows or that he himself particularly guards against in those other ventures of his where they are not nearly so dangerous as when he is trading in commodities or stocks.

The public ought always to keep in mind the elementals of stock trading. When a stock is going up no elaborate explanation is needed as to why it is going up. It takes continuous buying to make a stock keep going up. As long as it does so, with only small and natural reactions from time to time, it is a pretty safe proposition to trail with it.

But if after a long steady rise a stock turns and gradually begins to go down, with only occasionally small rallies, it is obvious that the line of least resistance has changed from upward to downward. Such being the case why should anyone ask for explanations? There are probably very good reasons why it should go down…

Gold reserves of European countries in tonnes

Great Trading Books -Just Read If U Have Time

Trading Psychology :

- “Trading to Win: The Psychology of Mastering the Markets”

- “Trading in the Zone: Maximizing Performance with Focus and Discipline”

- “The Psychology of Risk: Mastering Market Uncertainty”

- “The Mental Strategies of Top Traders: the Psychological Determinants of Trading Success”

- “Hedge Fund Masters: How top Hedge Funds Set Goals, Overcome Barriers and Achieve Peak Performance”

- “Mastering Trading Stress: Strategies for Maximizing Performance”

- Prior to his passing, I had been organizing a conference with Dr. Kiev. He revolutionized the hedge fund industry in terms of trader performance

- “Psychology of the Stock Market” – G.C. Selden

- The book was written in 1912, but offers great insight in stock market speculation.

- “On Managing Yourself” – Dr. Mario F. Conforti

- “As a Man Thinketh” – James Allen

- A timeless classic in my opinion.

- “Fighting Attachment in Trading” – Jon Ossoff (Active Trader, August 2011)

- “The Crowd: A Study of the Popular Mind” – Gustave Le Bon, 1896

- “Who Are You?” – Linda Bradford Raschke (SFO, Aug. / Sept. 2003)

- Linda has made a number of contributions to trading and I have utilized several of her general market observations and concepts.

- “Maintain Your Mindset: Using the Three R’s & Positive Thinking” – Linda Bradford Raschke (SFO, July 2004)

- “The Hour Between Dog and Wolf: Risk Taking, Gut Feelings and the Biology of Boom and Bust” – John Coates, 2012

- “Deny Your Inner Gamble Monkey” – MarketWatch.com (December 11, 2012)

- “Why Smart Traders Do Dumb Things: Understanding Prospect Theory” – David Silverman (SFO, July 2005)

- “Self-Attribution Bias in Consumer Financial Decision-Making: How Investment Returns Affect Individuals’ Belief in Skill” – Arvid O. I. Hoffmann Thomas Post

- “Conquering Sabotage Traps in Your Trading” – Adrienne Toghraie – INO.com

- “Five Guiding Principles of Trading Psychology” – Brett N. Steenbarger, Ph.D.

- Brett is one the must follows in the field of trading psychology. He has written so much on the topic and all is easily accessible on the web.

- “Explaining the Wisdom of Crowds: Applying the Logic of Diversity” – Michael J. Mauboussin (Legg Mason, Mar.2012)

- “The Playbook: An Inside Look at How to Think Like a Professional Trader” – Mike Bellafiore, 2014

- The most comprehensive book I’ve read on what it takes to become a professional trader. A lot of books talk about the concept, but this lays out a step-by-step blueprint. Very well written.