US equities snapped back to losses yesterday, though they finished off the lows at least. Futures are keeping mildly higher today but the overall mood remains more tepid as we start to move towards European morning trade.

The dollar is a touch softer but nothing significant, as major currencies are still keeping in rather narrow ranges for the most part today.

It is still going to be all about risk sentiment ahead of the weekend, so expect virus headlines to dominate once again to see if we can get more meaningful price action rather than the choppy back and forth we have been seeing since last week.

0900 GMT – Eurozone May construction output data

Prior release can be found here. Construction activity is expected to bounce back after bottoming out in April, but overall conditions should remain highly subdued still.

0900 GMT – Eurozone June final CPI figures

The preliminary report can be found here. As this is the final release, it shouldn’t have much – if any – impact to markets.

Also, at 0800 GMT we will be getting the latest ECB survey of professional of forecasters but it isn’t really much of a notable release.

That’s all for the session ahead. I wish you all the best of days to come and good luck with your trading! Stay safe out there.

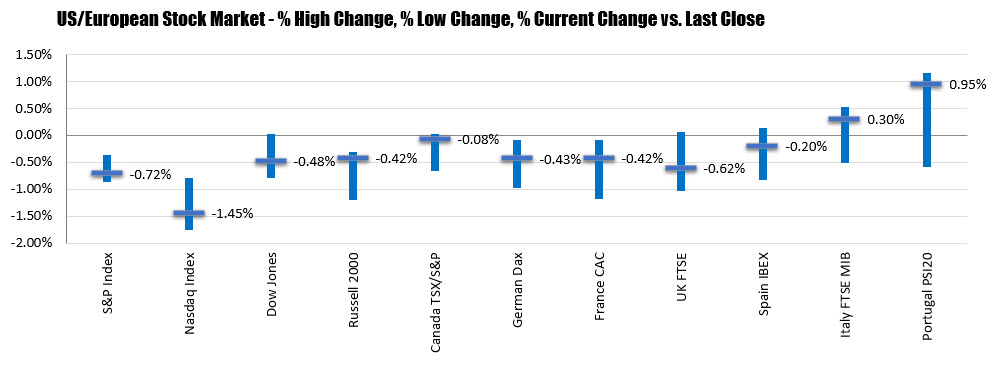

In other markets as London/European traders look to exit:

In other markets as London/European traders look to exit: