Deutsche Bank’s new research report now ranks #Bitcoin as the third largest currency in circulation.

highlights:

The final numbers area showing:

Wednesday, March 24

The major European indices are ending the session lower. For the week, the results are mixed:

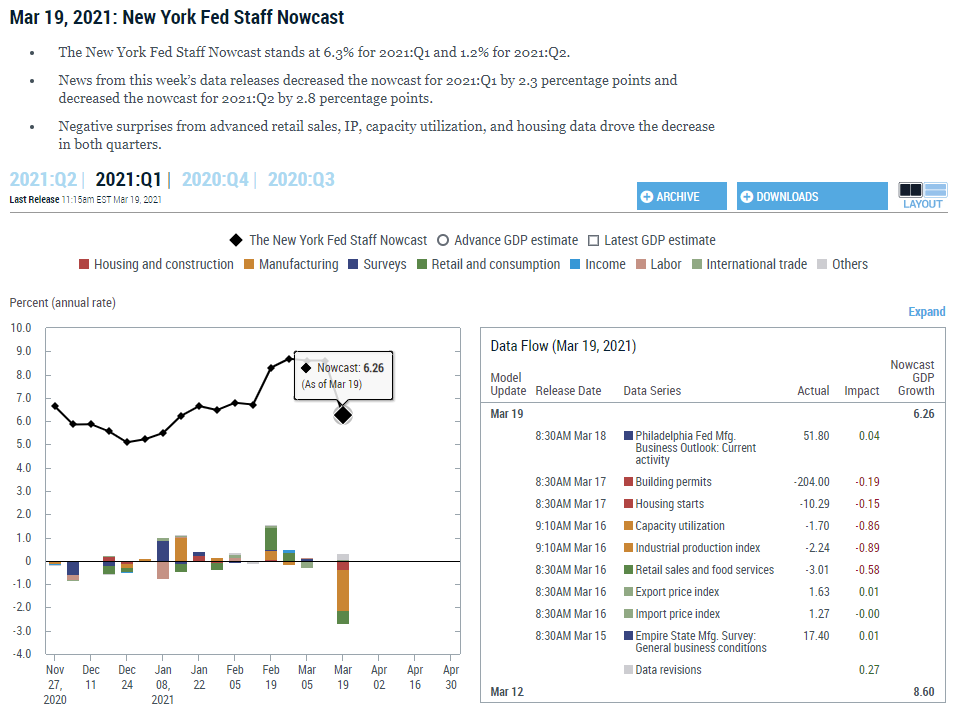

The fall in the NY Fed model, brings the estimate more in line with the Atlanta Fed model which pegs 1Q growth at 5.7%. They will announce a new estimate on March 24.

Standard economics assumes that we are rational—that we know all the pertinent information about out decisions, that we can calculate the value of the different options we face, that we are cognitively unhindered in weighing the ramifications of each potential choice. We are presumed to be making logical and sensible decisions. If we make a mistake, the supposition is that we will learn from those mistakes and behave differently in the future.

However, we are far less rational in our decision making than standard economic theory assumes. Our irrational behaviors are neither random nor senseless—they are systematic and predictable. We make the same types of mistakes repeatedly because of how our brains are wired. Behavioral economists believe that people are susceptible to irrelevant influences from their immediate environment, irrelevant emotions, shortsightedness, and other forms of irrationality.

What good news can accompany this realization? The good news is that these mistakes also provide opportunities for improvement. If we all make systematic mistakes in our decisions, then why not develop new strategies, tools, and methods to help us make better decisions and improve our overall well-being? [Behavioral economists believe] that there are tools, methods, and policies that can help all of us make better decisions and as a consequence achieve what we desire.

When it comes to the markets and our quest to understand them, we would all benefit from first learning about ourselves. Then, and only then, may we have a fighting chance to “trade another day”.

Just a thought.