ata to continue to play second fiddle to trade talks and Brexit headlines

Happy Friday, everyone! Hope you’re all doing well as we look to get things going in the session ahead. It’s been a calmer start to the day as markets are holding out optimism on trade talks in Washington and that has been the main theme playing out so far.

However, the pound was the standout performer in overnight trading after Brexit talks between UK PM Johnson and Irish PM Varadkar overshadowed the main focus of US-China trade talks. Cable holds above 1.2400 still on optimism of a watered-down Brexit deal.

Needless to say, I still reserve some skepticism over the matter because if this is what it boils down to, then why didn’t they just get on with it during Theresa May’s tenure rather than waste everyone’s time for the past year or so?

Looking ahead, it’s still all about the mood surrounding trade talks as Trump will be meeting with Liu He later on in the day. As such, trade headlines will continue to be the key factor driving trading sentiment as we look to wrap up the week.

0600 GMT – Germany September final CPI figures

The preliminary report can be found

here. As this is the final release, it isn’t going to offer much of anything new unless the figures deviate substantially from initial estimates.

0700 GMT – Spain September final CPI figures

Much like the above, as this is the final release, it isn’t going to offer much of anything new unless the figures deviate substantially from initial estimates.

That’s all for the session ahead. I wish you all the best of days to come and good luck with your trading!

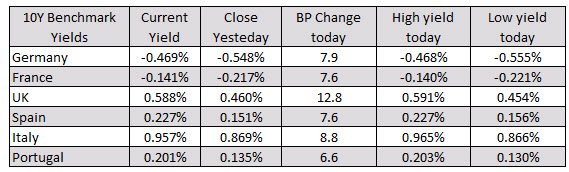

In the European debt market, yields have soared higher with the UK yield up the most at 12.8 basis points on hopes for a successful Brexit deal. The German yield is up 7.9 basis points. France’s yields are up 7.6 basis points.

In the European debt market, yields have soared higher with the UK yield up the most at 12.8 basis points on hopes for a successful Brexit deal. The German yield is up 7.9 basis points. France’s yields are up 7.6 basis points.