Late day selling hurts major indices

Some late day selling has pushed the major indices into the red. All the S&P sectors are closing lower on the day.

The final numbers are showing:

- S&P index -9.13 points or -0.28% to 3237.15. The high reached 3244.91.The low extended to 3232.43

- NASDAQ index fell -2.883 points or -0.03% to 9068.58. The high reached 9091.93. The low extended to 9042.55

- Dow fell -119.97 points or -0.42% to 28583.43. The high reached 28685.50. The low extended to 28565.28.

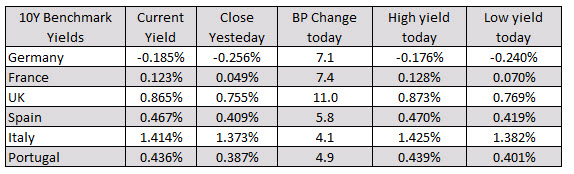

In other markets as European traders exit:

In other markets as European traders exit: