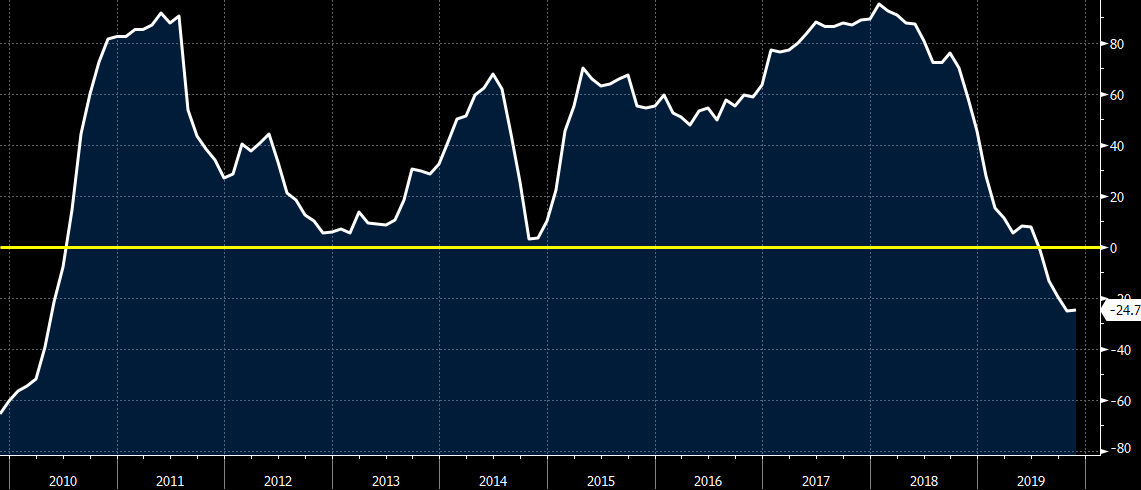

A total of 125 Japanese manufacturers have revised down their net profit forecasts for the current fiscal year by a sum of 939.3 billion yen ($8.6 billion), the largest collective downgrade in seven years, data compiled by Nikkei shows.

The wave of profit warnings stands in contrast to the upbeat forecasts of the nonmanufacturing sector, such as IT and services, and highlights the ripple effects of sluggish economic growth in China and other parts of the world.

Of the 171 manufacturing companies that have revised their earnings forecasts for the fiscal year ending March 31, 2020, about 70%, cut their forecasts, the largest proportion in seven years.

Upward revisions have totaled just 272.9 billion yen so far this fiscal year.

The downward revisions have already exceeded last year’s total of 832.5 billion yen. The total is the highest since 2012, when the figure reached 2.21 trillion yen.

The profit outlook for this fiscal year stands to get worse. Only 30% of companies have so far announced earnings results for the April-September period, indicating that the total figure for downgrades of profit outlooks could go much higher.

The auto industry felt the impact of slowing economic growth in China and elsewhere in the world. “The Chinese market is still tough, and its state is unclear,” said Ryuichi Umeshita, an executive at Mazda Motor, at a news conference on Friday. “The U.S. in the mass-market price range is also a struggle.” The company now expects net profit for the current year to decline to nearly 43 billion yen, just about half the previous forecast of 80 billion yen.

Suzuki Motor also cut its net profit forecast to below last year’s levels due to weak four-wheeler sales in India. Hino Motors sees sluggish sales in Asia. “The recovery in overseas demand has generally been slow,” said CEO Yoshio Shimo. Major automotive parts supplier Aisin Seiki has seen s fall off in demand for transmissions among local manufacturers in China.

Other manufacturers are being hit from a decline in corporate investment.

Mitsubishi Electric’s factory automation equipment sales are weak. “The demand for smartphones and 5G that was expected to recover in the second half of the year is likely to be pushed back,” said Tadashi Kawagoishi, a director at Mitsubishi Electric.

Hiroyuki Ogawa, President and CEO of Komatsu, said the scale of the decline in sales of construction machinery in China and elsewhere in Asia is “unexpected.”

In the nonmanufacturing industry, by contrast, more companies have revised their profit forecast upward than downward, led by solid earnings among small and medium enterprises.

As of early October, total net profits for Japanese companies was expected to be flat compared with the previous year. But if the downturn in manufacturing, which accounts for large share of profits, continues at this pace, the figure may decline for the second consecutive year.