Russell 2000 falls -2.8%

The Dow is closing at a record close. The Nasdaq lagged with the Russell 2000 of small-cap stocks taking it on the chin.

The final numbers are showing:

- S&P index fell -3.35 points or -0.08% at 3971.19

- Nasdaq fell -79.07 points or -0.60% at 13059.64

- Dow rose 98.43 points or 0.3% at 33171.31

- The small-cap Russell 2000 fell -62.8 points or -2.83% at 2158.50.

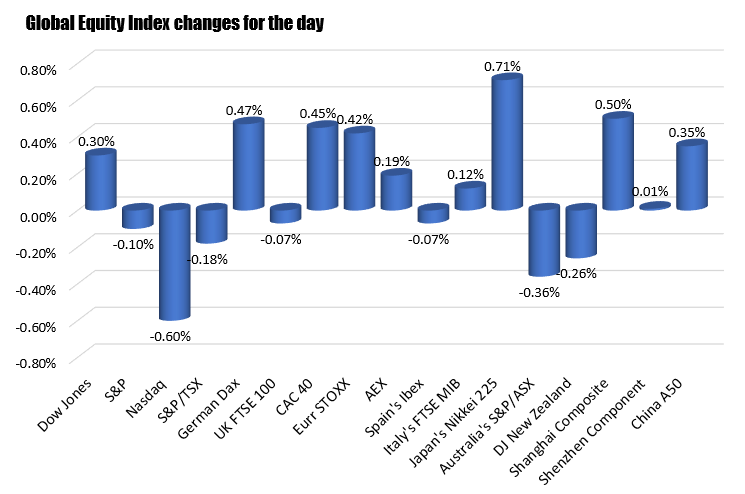

Below is a summary of him the % changes for the major global indices to start the trading week:

Yields rose with the yield curve steepening in the US today which has tended to weaken the high tech growth stocks.

- 2 year rose 0.7 basis points to 0.140%

- 10 year rose 3.3 basis points to 1.709%

- 30 year rose 3.0 basis points to 2.408%