This headline is inevitable.

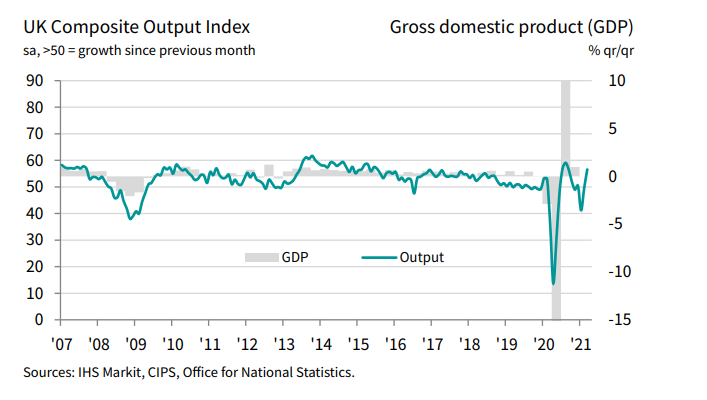

Business activity in the UK returned to expansion and improved at its quickest pace in seven months, with the services reading also coming in at the highest since August last year. Meanwhile, the manufacturing reading is the highest in 40 months.

“The UK economy rebounded from two months of decline in March, with business activity growing at its fastest rate since last August as children returned to schools, businesses prepared for the reopening of the economy and the vaccine roll-out boosted confidence. Companies reported an influx of new orders on a scale exceeded only once in almost four years, and business expectations for growth in the year ahead surged to the highest since comparable data were first available in 2012. Employment consequently rose for the first time since the pandemic struck as firms expanded capacity in response to the new inflows of work and brighter outlook.

“The surge in business activity is far stronger than any economists expected, according to Reuters polls, and hints at only a modest contraction of GDP during the first quarter, adding to evidence that the economy has shown far greater resilience in the third lockdown compared to the first. The encouraging readings on future expectations, job creation and new order inflows meanwhile all point to robust economic growth in the second quarter, especially if virus restrictions are lifted further.

“Worries persist though, especially in relation to near-record supply chain delays, a continued fall in exports and sharply rising prices, all of which are making life difficult for many companies. Many consumer facing companies meanwhile remain constrained by COVID-19 restrictions, which are likely to curb the overall pace of economic growth for some time to come, especially if we see a third wave of infections.”

The French and German readings set out what to expect here and it is largely positive, with the services reading coming in at a 7-month high while the manufacturing reading is a record high for the overall Eurozone.

“The eurozone economy beat expectations in March, showing a much better than anticipated expansion thanks mainly to a record surge in manufacturing output.

“The service sector remains the economy’s weak spot, but even here the rate of decline moderated in March as companies benefited from the manufacturing sector’s upturn, customers adapted to life during a pandemic and prospects remained relatively upbeat.

“The outlook has deteriorated, however, amid rising COVID-19 infection rates and new lockdown measures. This two-speed nature of the economy will therefore likely persist for some time to come, as manufacturers benefit from a recovery in global demand but consumer-facing service companies remain constrained by social distancing restrictions.

“The surge in demand for manufactured goods is meanwhile stretching supply chains to an unprecedented extent, in turn pushing costs up at the fastest rate for a decade. These cost pressures will likely feed through to higher consumer price inflation in coming months.”

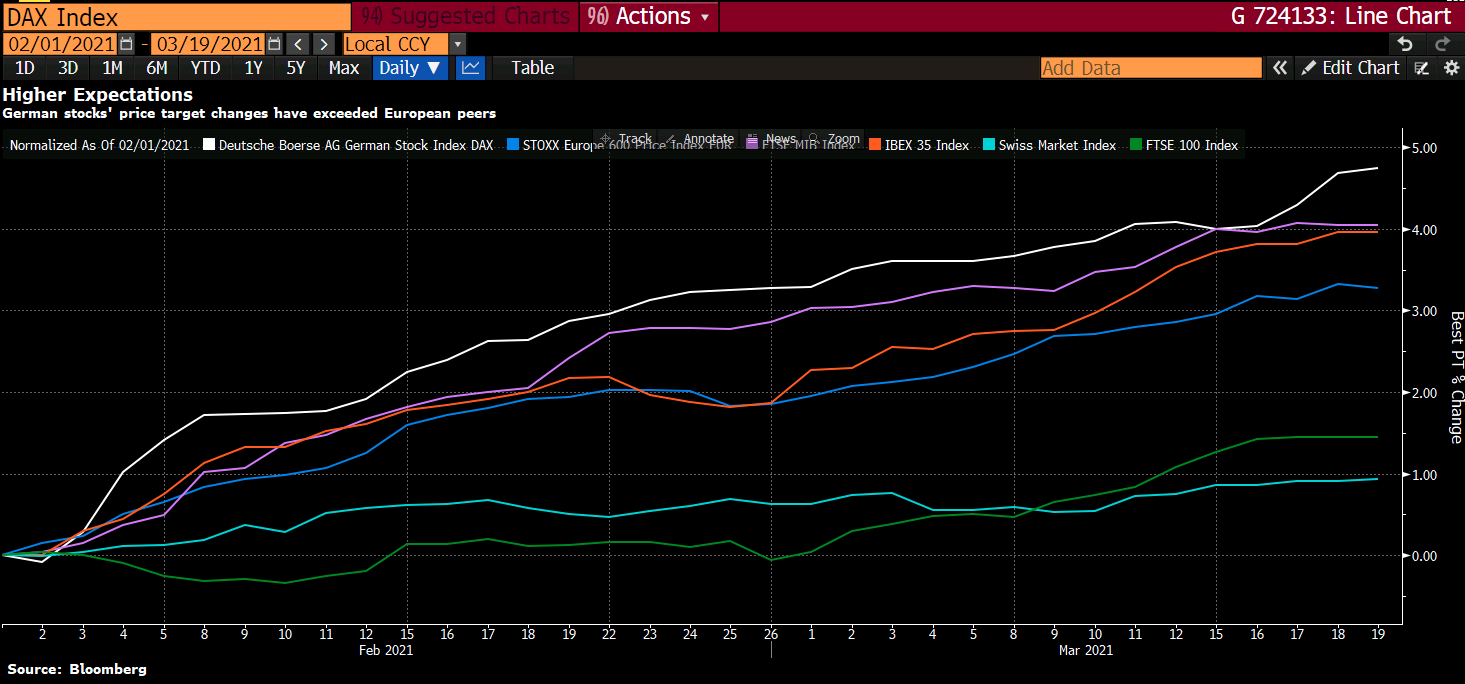

The surge in Volkswagen shares last week that helped German stocks higher underlines the DAX as a cyclical recovery play.

The DAX outperformed European stocks overall last week with the DAX edging ahead of the FTSE MIB. A large part of the rally has been as Volkswagen bids to rival Tesla in electric vehicles. Volkswagen overtook SAP as Germany’s most valuable public company. The slowdown in Germany remains as the vaccine rollouts are dogged by delay. Eventually, though, the recovery should come to Germany. That is of course with all the caveats that we currently have regarding how the variants will develop and the pandemic proceed.

Bloomberg survey puts DAX ahead of the European pack

On average the anticipated gain is 2% by the end of the year. This is slightly more than in February. Since the start of February the DAX’s 12 month forward price target percent change has moved ahead of other European peers. Check out the comparison below:

Today is not the best day to chase this as the reflation trade is having a wobble. Whether it is a deeper pullback in equities or not is uncertain, but there is a bit or re-orientation going on right now.

Today is not the best day to chase this as the reflation trade is having a wobble. Whether it is a deeper pullback in equities or not is uncertain, but there is a bit or re-orientation going on right now.

PBOC injects 10 billion yuan liquidity via 7-day reverse repo