Comparing Panama Papers to other leaks.

But let’s use a couple of examples:

– trading: I buy a basket of stocks this morning with the intention of reselling before the close

– investing: I build a portfolio of stocks with the intention to keep it a relatively long time, because I think that these stocks value will increase due to whatever reason, growth, value, the economy…

I also like the following classification, which I believe comes from Minsky:

– Profits on the position neither depend on price variation of the asset, nor on cost of carry: I am investing.

– Profits do not depend on price variation, but only on positive carry: I am trading.

– Profit depend on price variation of the asset: I am speculating.

The example and the definition are not equivalent, but they give a rough idea of what trading is and what investing is. The border between both activities can be blurry. But if you invest, you do not need a market. You can buy a bond with the intention of holding it to maturity. If you trade, you need a market to close the trades.

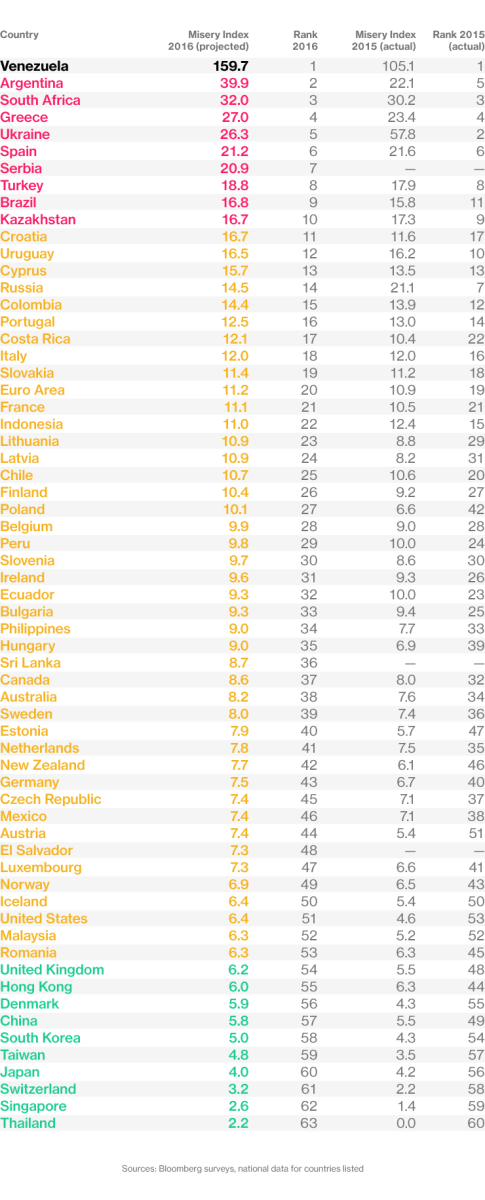

Just Click to Enlarge

Let’s turn those problem-focused questions into solution-focused ones:

* When have I been trading with good discipline? What do I do differently at those times?

* When have I executed trades well? What helped me find good prices for my entries?

* When have I done a good job managing the risk of a particular trade or a particular trading day? What did I draw upon to implement good risk management? (more…)

And the great sea with its friends and its enemies. And bed, he thought. Bed is my friend. Just bed, he thought. Bed will be a great thing. It is easy when you are beaten, he thought. I never knew how easy it was. And what beat you, he thought. ‘Nothing’, he said aloud. ‘I went out too far.’

– Hemingway, The Old Man and the Sea

‘At that point I ought to have gone away, but a strange sensation rose up in me, a sort of defiance of fate, a desire to challenge it, to put out my tongue at it. I laid down the largest stake allowed – four thousand gulden – and lost it. Then, getting hot, I pulled out all I had left, staked it on the same number, and lost again, after which I walked away from the table as though I were stunned. I could not even grasp what had happened to me.’

– The Gambler, by Fyodor Dostoevsky

If you must play, decide upon three things at the start: the rules of the game, the stakes, and the quitting time.

– Chinese Proverb

Luck never gives; it only lends.

– Swedish Proverb

Depend on the rabbit’s foot if you will, but remember it didn’t work for the rabbit.

– R.E. Shay

Over the last twenty-five years, there has been a lot of interest in herd behavior in financial markets—that is, a trader’s decision to disregard her private information to follow the behavior of the crowd. A large theoretical literature has identified abstract mechanisms through which herding can arise, even in a world where people are fully rational. Until now, however, the empirical work on herding has been completely disconnected from this theoretical analysis; it simply looked for statistical evidence of trade clustering and, when that evidence was present, interpreted the clustering as herd behavior. However, since decision clustering may be the result of something other than herding—such as the common reaction to public announcements—the existing empirical literature cannot distinguish “spurious” herding from “true” herd behavior.

Over the last twenty-five years, there has been a lot of interest in herd behavior in financial markets—that is, a trader’s decision to disregard her private information to follow the behavior of the crowd. A large theoretical literature has identified abstract mechanisms through which herding can arise, even in a world where people are fully rational. Until now, however, the empirical work on herding has been completely disconnected from this theoretical analysis; it simply looked for statistical evidence of trade clustering and, when that evidence was present, interpreted the clustering as herd behavior. However, since decision clustering may be the result of something other than herding—such as the common reaction to public announcements—the existing empirical literature cannot distinguish “spurious” herding from “true” herd behavior.

In this post, we describe a novel approach to measuring herding in financial markets, which we employed in a recently published paper. We develop a theoretical model of herd behavior that, in contrast to the existing theoretical literature, can be brought to the data, and we show how to estimate it using financial markets transaction data. The estimation strategy allows us to distinguish “real” herding from “spurious herding,” or the simple clustering of trading behavior. Our approach allows researchers to gauge the importance of herding in a financial market and to assess the inefficiency in the process of price discovery that herding causes.

The Model

Let’s give an overview of the model that we brought to the data and try to explain why herding would arise. In the model, an asset is traded over many days; at the beginning of each day, an event may occur that changes the fundamental value of the asset. If an event occurs, some traders (informed traders) receive (private) information on the new asset value; although this information may be imprecise, these traders do know that something occurred in the market to alter the value of the asset. The other traders in the market trade for reasons not related to information, such as liquidity or hedging motives. If no event occurs, all traders only trade for non-informational reasons. (more…)