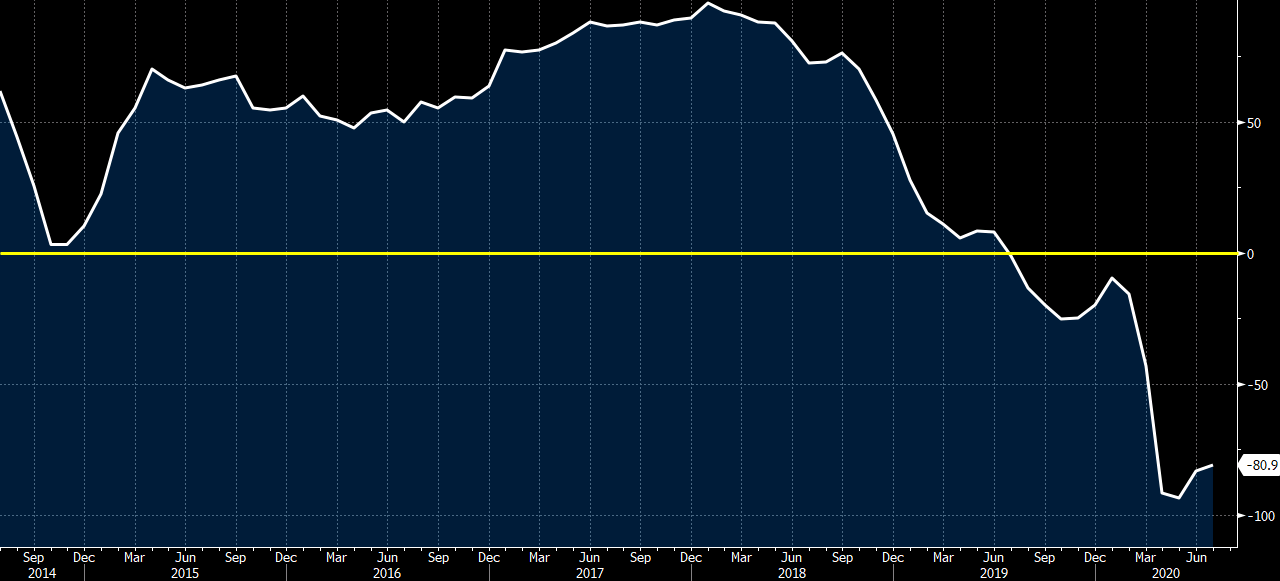

Latest data released by ZEW – 14 July 2020

- Prior -83.1

- Expectations 59.6 vs 60.0 expected

- Prior 63.4

What stands out in this report here is that any rebound in economic sentiment remains tepid at best and while expectations are still elevated, they have dropped off slightly – a hint that optimism about the future is becoming more measured.

On the latter, it would be a focal point moving forward as that will more or less give an idea about the pace of the recovery and this early stutter isn’t all too encouraging.