FAAANM performance since 2015.

Saudi Arabia is proposing to move the OPEC meeting to mid June. This according to a OPEC delegate. The delay to OPEC meeting would allow time to review the May production and compliance data.

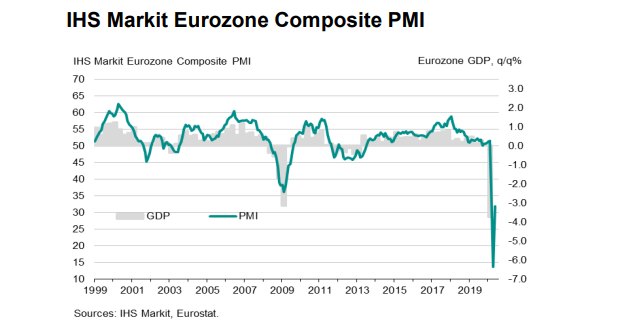

“The scale and breadth of the eurozone downturn was highlighted by the PMI data showing all countries enduring another month of sharply falling business activity. Eurozone GDP is consequently set to fall at an unprecedented rate in the second quarter, accompanied by the largest rise in unemployment seen in the history of the euro area.

“Encouragingly, while rates of decline of both business activity and employment remained shockingly steep for a third successive month in May, the downturn has already eased markedly in all countries surveyed. Optimism about the outlook has also returned in Italy and, to a lesser degree, France, while pessimism has moderated markedly in all other countries.

“Providing there is no resurgence of infection numbers, the planned lifting of lockdowns will inevitably help boost business activity and sentiment further in coming months.

“However, the outlook is scarred by the prospect of demand remaining weak due to household spending being hit by high levels of unemployment and corporate spending being subdued as companies repair balance sheets.

“Consumer-facing services are likely to continue to take the hardest hit from those COVID-19 containment measures that may need to stay in place the longest, acting as a particular drag on the overall recovery.

“We therefore remain cautious with respect to the recovery. Our forecasters expect GDP to slump by almost 9% in 2020 and for a recovery to prepandemic levels of output to take several years.”

After that that came more from the outspoken media group:

the US major indices are closing near session highs. The Dow industrial average led the index is charged with a 1.05% gain. S&P and NASDAQ posts the 6th gain in 7 trading days. The NASDAQ index is closing lesson 3% from the record high set in February.