The US-China trade war drags on

Where the economies of US and China go, the rest of the world economies follow. Why is that? Well, around 40% of the world’s

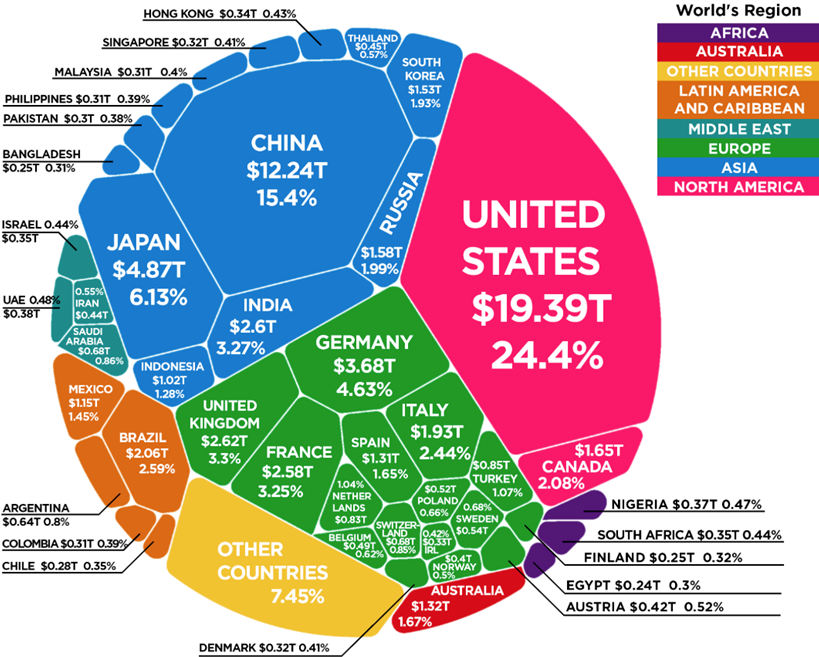

GDP comes from the combined economies of the US and China.

Take a look at the chart below from the World Economic Forum and you will see how a large proportion of the world’s $80 trillion GDP is made up by the US and China’s economies.

So, the market’s concern with the ongoing US-China trade dispute is really an ongoing concern about global growth. That is why a fall out between the US and China impact global financial markets.

The market wants the US-China trade dispute resolved as soon as possible. The markets have become used to a game of ‘ping-pong’ where some news prompts optimism about a US-China trade deal and then some other, conflicting news, encourages pessimism about the US-China trade deal. It’s truly a game of geo-political ping pong!

At the moment the market is digesting the latest news on Tuesday last week where US President Trump announced that it is probably better to wait until after the 2020 presidential election for a China deal and that there is no timeline on trade.

Then, on Wednesday, some sources quoted by Bloomberg said that a deal was much closer than the recent heated dialogue would otherwise indicate. Another game of ping pong! However, it is worth being aware that the US-China trade dispute could actually get much worse.

Two of the ways it could deteriorate would be if the US goes ahead with restricting US capital flows into China and if the impact of the Hong Kong riots spill over to further political moves from the US or China.

The impact of proposals to restrict US capital flows into China

One of the moves the US has suggested at the end of September this year in the ongoing

trade war is a restriction of US capital flows into China. To literally turn off the tap of US capital. The impact of such restrictions could be:

- A drag on Chinese firms listed on global stock exchanges. Chinese companies listed on the US stock exchanges have a market capitalization of $1.3 trillion and include names like Alibaba and Beijing Capital Airport ADR.

- China may retaliate to the US restrictions and sell off some if it’s $1.2 trillion dollars of US debt. This would cause US bond prices to fall and yields to spike as an alarm response. This in turn would make it costlier for US companies and consumers to borrow. A complete selling of US debt would be enormously risky for China as they are the largest foreign creditors of debt.

- There is a danger of a decoupling between the US and Chinese economies and that would cause a far greater impact than the tariffs already in place have.

Hong Kong turmoil adds to tensions

The relationship between Hong Kong and China is tense. There is a ‘one country, two system’s’ policy between Hong Kong and mainland china, but the relationship is under strain. The catalyst for the strain has been Hong Kong protests over a proposed Chinese law to allow the extradition of criminal suspects to mainland China.

This has been the source of all the problems and riots that have been taking place recently. To make matter worse, at the end of November, President Trump signed new human rights legislation authorising sanctions on Chinese and Hong King officials responsible for human rights abuses in Hong Kong.

In this way the US are signaling support for pro-democracy activists. China responded to this legislation by calling it an illegal interference in its own affairs. The current expectations are that this in itself is not enough to de-rail US-China trade talks and Donald Trump.

However, it is an added tension in an already difficult relationship. President Trump has tried to avoid antagonising the situation by signing the bill in private and not having a large press conference.

However, there are certain predictable responses that the market makes when it is concerned. These moves are called ‘

risk off’ moves. In a risk off market we typically see gold strength,

JPY and

CHF strength,

US oil weakness, bonds bid,

AUD, JPY, and equity weakness.

Gold

A US-China trade war will make

gold an attractive asset to buy. A world with central banks having

low interest rates and risk being elevated makes gold a decent potential for investors seeking alpha. Also, with the month of January being an excellent time for gold, over the last decade, a breakdown in US-China trade relations would further encourage

gold bulls.

Yen

The Japanese Yen is a traditional safe haven currency. Negative interest rates, like the Bank of Japan currently has, would typically discourage currency capital inflows. However, the debt structuring of Japan means that the currency is considered very stable and safe for uncertain times. As a result, when investors and speculators are fearful, there are sudden and marked inflows into the Japanese Yen.

The pair that stands out for particular downside in a fresh round of the ongoing US-China trade war would be the AUD/JPY pair. As around 30% of Australia’s economy is made up of trade with China it stands to lose out on a US-China trade war. Further trade strain would result in AUD weakness and JPY strength on safe haven flows.