A rough day for Japanese stocks, particularly in the closing hour

Asian equities have turned more sour as the risk mood softens ahead of European trading today. It is a new month and new quarter, so fresh flows and sentiment will be evident after talk of re-balancing action over the past week.

Concerns of the virus outbreak becoming more widespread in Japan and the continued economic fallout globally is stoking fears among investors it seems.

The Hang Seng is down by over 2% while Chinese equities have also seen earlier gains – largely on the back of stimulus hopes – fade with the Shanghai Composite also down at the lows now, falling by 0.3% going into the final hour of trading.

US futures are down by over 3% currently and that is setting a bit of a softer tone to start the session. USD/JPY is keeping a little lower at 107.36 as such.

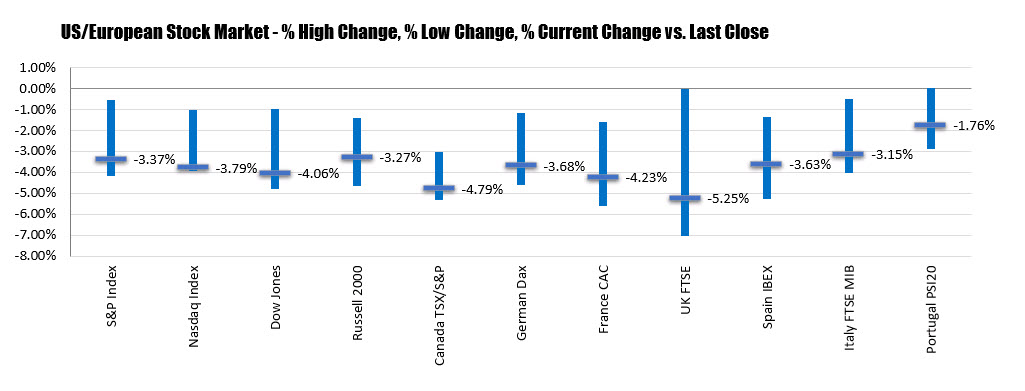

Although lower for the day for all major indices closed with gains.

Although lower for the day for all major indices closed with gains.