50 COGNITIVE BIASES

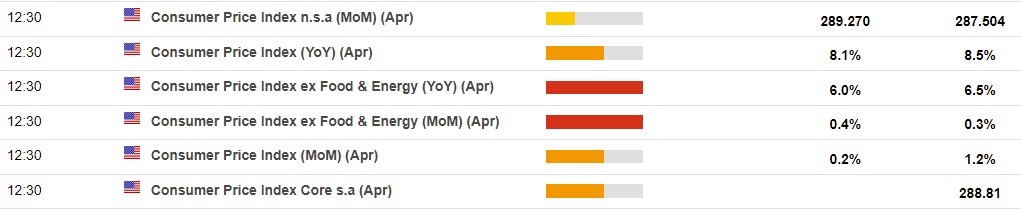

US CPI data due today, 1230 GMT:

Some relief is the consensus expectations, snippets from analysts:

Société Générale:

BNZ:

NAB:

ING:

An ICYMI from Fitch rating agency overnight, with comments that will take no one by surprise.

In brief:

The major US indices are ending the day mixed results. The Dow industrial average is down. The S&P index is modestly higher, while the NASDAQ is up nearly 1%. Yesterday the major indices all fell sharply to start the trading week.

A look at the final numbers shows:

All the major indices had their share of ups and downs today as the market consolidated the sharp declines from yesterday’s trade. The NASDAQ index did trade to a new year low at 11566.28. That took out the low price from yesterday at 11574.94.

The S&P and Dow industrial average also made new 2022 lows. For the S&P, it reached 3958.17 taking out the low price from yesterday at 3975.48. For the Dow industrial average traded to a new low of 31887.89, after trading to a low yesterday of 32121.9.

In after-hours trading Coinbase reporting much worse than expected earnings of -$1.98 vs. expectations of +$0.18. Revenues came in at $1.17 billion vs. expectations of $1.48 billion. Monthly transacting users came in at 9.2 million vs. 9.5 million expected.

The stock is currently trading at $65.07 down -$7.92 or -10.85%. That comes after trading down -$10.52 or -12.6% in the normal trading hours today. Yesterday the stock closed at $83.51.

Year-to-date COIN is down 70.93%. The high for the year was the 1st day of the year at $251.