From 1923 (Truth of the Stock Tape – Gann) – great page and I underlined some key points.

.jpg)

The weekend is a perfect time for a quick catch up for where the major central banks are at. The central banks are listed below with their current state of play. The link for each central bank is included under the title of the bank and the next scheduled meeting is in the title too.

Reserve Bank of Australia, Governor Phillip Lowe, 0.25%,Meets June 02

At their last meeting the RBA has kept interest rates unchanged at the record low if 0.25%. The RBA see output falling by approximately 6% this year, but expects a 6% rebound next year. At the last set of minutes on May 19 the Board said the they are monitoring economic and financial developments. See here for a decent summary of where the RBA are at.

The last thing to note is that the Australian economy is closely tied to China’s fortunes with around 30% of its GDP coming from trade with China. Therefore, AUD will be pushed or pulled along with the US-China trade sentiment too as well as monetary policy. Any further souring in the US-China risk tone will weaken the outlook for AUD, so bear that in mind.

European Central Bank, President Christine Lagarde, 0.00%, Meets June 04

The outlook for the eurozone remains tilted firmly to the downside with inflation levels in March remaining below the 2% target at 0.7%. Unemployment levels stand at 7.3% and the ECB has embarked upon a huge programme of support via it’s Pandemic Emergency Purchase Programme (PEPP). Early this month the German’s Constitutional Court ruled that the ECB had to show that this programme was proportionate. However, the significance of this ruling has faded after Germany downplayed any deeper significance. In April the ECB kept all three key rates unchanged, but released a series of pandemic emergency longer term refinancing operations (PELTROs) and they further eased conditions of TLTRO3. Like many central banks the ECB will maintain a dovish tilt, willing to do more if necessary to ease conditions, until the worst of the COVID19 can be seen to be well and truly behind us. The latest minutes from April 30th’s meeting confirm that the ECB are ready to do more and that the PEPP remains the main tool.

Bank of Canada, Governor Stephen Poloz, 0.25%, Meets June 03

The bank of Canada left their rates unchanged in April and announced a stimulus package in the form of a new Provincial Bond Purchase Programme. The future economic forecasts were sensibly omitted but various scenarios suggested by the BoC had the level of real activity down 1-3 percent in the first quarter of 2020. It isalso anticipated to be 15-30 percent lower in the second quarter of 2020 than in fourth-quarter 2019. See here for more details on the Interest rate decision. The current Governor is due to leave at the end of his 7 year term and the new successor is Tiff Macklem. You can read his bio here on the Bank of Canada website.

Federal Reserve, Chair: Jerome Powell,0.00%-0.25%. Meets June 10

The FOMC left rates unchanged at their latest meeting and Fed’s Chair Jerome Powell was deliberate in talking down the chances of negative interest rates. The Fed have kept their willingness to step into help the economy in any way they can as well as discussing the possibility of yield curve controls in case rates wobble in a certain sector. The latest minutes showed the Fed expected the pace of treasury and MBS purchases could be reduced but said it was prepared to increase purchases as needed should market functioning worsen. There was some debate about how to show forward guidance to the market going forward, Some members said that the Fed could adopt an outcome based forward guidance. This method would specify macroeconomic outcomes such as a certain level of the unemployment rate or level of inflation rate before rates could be increased. Other members considered a date based forward guidance . This method would indicate that interest rateswould only be raised after a specified amount of time had passed. The OIS curve for Fed Fund Futures are pointing towards rates remaining unchanged over the next 12 months, but risks remain tilted to the downside. Any positive talk of negative interest rates from the Fed will weaken the dollar. A great commodity to potentially benefit would be gold which gains in a low interest rate environment. If risk is off market increases, and that forces the Fed’s hand to try negative rates, then gold should strongly rally higher and break out to make record highs.

Bank of England, Governor Andrew Bailey, 0.10%, Meets June 18

Once again the storm cloud which continues to obscure the BoE’s view is Brexit. The problem is that a greater storm cloud is now obscuring that! COVID-19. The UK was cavalier in its attitude to the virus and not helped by some main stream BBC articles comparing COVID-19 to the flu. I remember sharing my concerns over COVID19 to my friends and the general UK mood was one of disbelief. This laissez faire attitude resulted in the UK being very slow to bring in lock down measures and as other countries were shutting down the UK was talking about ‘Herd immunity’. Although hat quickly changed the damage was done. The UK now has the second official highest death count in the world, only behind the US.The BoE kept interest rates unchanged at 0.10% in April. Their asset purchase programme were kept at £645 billion withMPC members Saunders and Haskel surprising markets by voting for an increase in QE of £100 billion.

The BoE stated they stand ready to take further action as needed, but noted that indicators on UK demand have stabilised.The bank expects a relatively rapid recovery in economic activity with a rate hike and inflation returning to its 2% target by 2022. However, since the last central bank meeting Bank of England’s Deputy Governor Dave Ramsden said that ‘ an economic recovery later this year could be slower than in the BOE’s scenario published earlier this month and he pointed to several risks of long-term damage. Furthermore, Bank of England’s Bailey admitted that negative interest rates were on the table for the first time.This will weigh on the GBP alongside the fact that the UK has some of the world’s highest death figures for COVID19 and the EU-UK trade deal is still far from being finalised. We can expect more GBP sellers on pullbacks given these three factors weighing on the GBP.

Swiss National Bank,Chair: Thomas Jordan, -0.75%, Meets June 18

The SNB interest rates are the world’s lowest at-0.75% and haven’t changed at a scheduled meeting since 2009. However, with the strengthening Franc hurting the Swiss export economy a number of large institutions, like UBS Group, Raiffeisen Bank International AG and Bank J. Safra Sarasin, had been calling for a rate cut for Autumn of last year. However, these calls were ignored but the Swiss franc is only getting stronger with the safe haven flows Brough about by COVID-19. At their last meeting in March the SNB kept rates unchanged. However, they changed their tiering system saying they would raise the exemption threshold on negative rates from 25 times to 30 times the minimum reserve requirement from April 1st. As a potential warning sign the SNB revised its view of CHF from “highly valued” to “even more highly valued” . SNB Sight deposits, showing evidence ofSNB intervention by buying Euros and Dollars, have increased considerably in recent weeks. Check out this helpful graph below showing how SNB sight deposits are increasing as the EURCHF moved to 105.00. Is this the new so called ‘soft floor’?Source here.One thing is certain, don’t bet on it.

Bank of Japan, Governor Haruhiko Kuroda, -0.10%, Meets June 16

The Bank of Japan is very bearish as a bank. Inflation in Japan continues to miss the 2% target and the BoJ have stated that they will ‘keep very low interest rate levels for an extended period of time’. In April the bank kept the interest rate unchanged at -0.10% and the long term yield target at 0%. However, to help with economic conditions, they did remove QE limits for buying Japanese Government Bonds (JGBs). Furthermore, they accelerated corporate bond purchases to ease conditions. In their unscheduled meeting on May 22 they kept policy settings unchanged and decided on a new loan scheme aimed at boosting support to small/mid sized firms hot by COVID-19.

Reserve Bank of New Zealand, Governor Adrian Orr, 0.25%, Meets June 24,

The RBNZ has been keeping markets guessing over its use of negative interest rates. At their last policy meeting the RBNZ Monetary Policy Committee agreed to significantly expand the Large Scale Asset Purchase (LSAP) programme potential to $60 billion. However, this was expected. It was the possibility of negative interest rates which caused the most damage to the kiwi at the time when Deputy Governor Geoff Bascand clarified that the RBNZ would like to be ready for negative rates by the end of the year. It was this willingness for the RBNZ to allow negative interest rates which weakened the NZD at the time. However, fast forward a week or so later and Governor Orr dialled back expectations of negative rates. The RBNZ are widely expected to keep its OCR unchanged in the immediate future. However, the OIS curve would now suggest the odds of further easing will gradually increase as the months pass, but stay above 0 for the next 12 months.

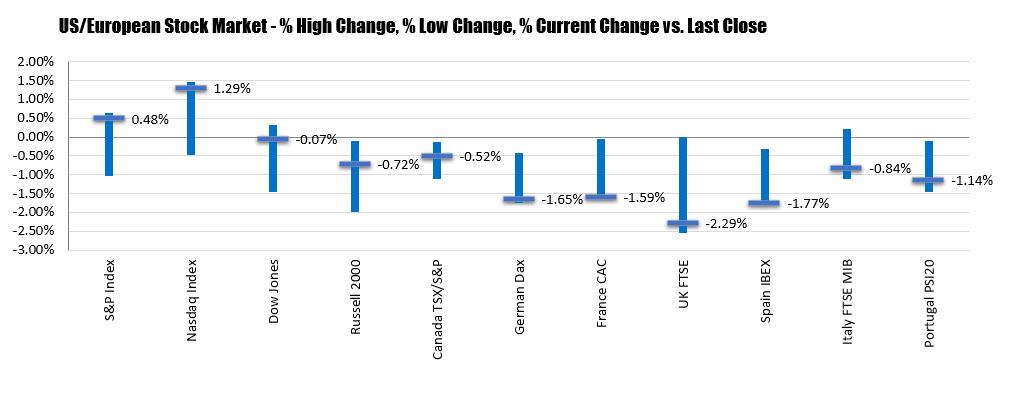

For the trading week, the Dow industrial average led the way with a 3.71% gain in the US. The NASDAQ index lagged as earlier in the week the flow funds were into the more beaten down industrial stocks. Nevertheless the NASDAQ gained by 2.21%. The S&P index rose by 3.25%.

For the trading week, the Dow industrial average led the way with a 3.71% gain in the US. The NASDAQ index lagged as earlier in the week the flow funds were into the more beaten down industrial stocks. Nevertheless the NASDAQ gained by 2.21%. The S&P index rose by 3.25%.Highlights for the week: