UK December CPI data in focus today

Good day, everyone! Hope you’re all doing well as we look to get things going in the session ahead. Markets are keeping more calm after a minor hiccup yesterday over tariff headlines but the main focus remains on the US-China trade deal signing later today.

Major currencies remain little changed thus far as the more steady tones are giving little direction for traders to work with in general. Looking ahead, we’ll have a couple of data points to move things along with the big one being UK inflation data.

0745 GMT – France December final CPI figures

The preliminary release can be found here. As this is the final release, it shouldn’t have much of an impact as it should reaffirm a slight rebound in price pressures last month.

0800 GMT – Spain December final CPI figures

The preliminary release can be found here. Similar to the French release, it should just reaffirm a slight rebound in inflation across the region last month.

0930 GMT – UK December CPI figures

0930 GMT – UK December PPI figures

Prior release can be found here. Price pressures in the UK is expected to keep more steady last month, but still below the desired 2% level. I reckon barring any significant drop-off in inflation, the BOE could lean towards staying pat in January but markets may still allude to this as being a reason to cut as well. In my view, post-election data matters more for the BOE so more steady price pressures (for now) should keep the finger off the trigger.

1000 GMT – Eurozone November industrial production

Prior release can be found here. The bounce in German industrial production for November should help give a slight nudge higher in the release here today but overall factory activity remains rather subdued in the euro area towards the end of 2019. A minor data point.

1000 GMT – Eurozone November trade balance data

Prior release can be found here. A general indication of trade conditions in the euro area economy, which is still a bit shaky in general amid slower global activity.

1200 GMT – US MBA mortgage approvals w.e. 10 January

Weekly US housing data, measures the change in number of applications for mortgages backed by the MBA during the week. Not the biggest of data points, but a general indicator of the housing sector sentiment.

That’s all for the session ahead. I wish you all the best of days to come and good luck with your trading!

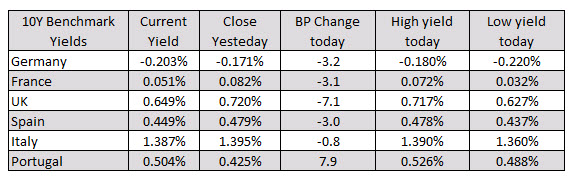

In other markets as London/European traders look to exit for the day (and just ahead of the ceremonial signing of the US/China phase 1 trade deal):

In other markets as London/European traders look to exit for the day (and just ahead of the ceremonial signing of the US/China phase 1 trade deal):