EBITDA (earnings before interest expenses, taxes, depreciation and amortization): Earnings before I tricked the dumb auditor.

EBIT (earnings before interest expenses and taxes): Earnings before irregularities and tampering.

EBITDA (earnings before interest expenses, taxes, depreciation and amortization): Earnings before I tricked the dumb auditor.

EBIT (earnings before interest expenses and taxes): Earnings before irregularities and tampering.

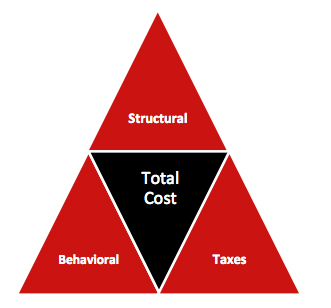

Rick Ferri has a new book coming out that I can’t wait to read. In the meantime, here’s something he put together illustrating the three costs that investors must control if they’re going to be successful…

Figure 1: The Investment Cost Triangle with Components

Some costs in Figure 1 are easy to identify and quantify while others are not. Structural costs are generally available because most fund fees and expenses are required to be disclosed by law. However, tax costs are more difficult in that they have to be extracted from tax return data. Behavioral costs are the most elusive and difficult to quantify because there’s very little data available. It also doesn’t help that human beings are overconfident and don’t want to be reminded of behavioral shortcomings.

Read the rest, this is the important stuff – much more important than the latest macro opinions on Greece or Guernica.

If dropping “ebitda” into cocktail party conversation makes you feel like a globetrotting financier, there is something you should know. It makes you sound like a MBA twit-clone with a Hermès tie and two brain cells. A fuzzy proxy for cash flow, ebitda (for the uninitiated, earnings before interest, tax, depreciation and amortisation) is the unit that investors and analysts reflexively use to talk about profit. (And what else do they talk about? Property?) It can mislead – but shouldn’t be abandoned.

The elegance of ebitda is that it comes straight off the income statement, and very high up on it where it should be purest. Coming ahead of interest expense, it is capital structure agnostic, and takes out recurring non-cash charges, too. But relying on the income statement alone ignores critical uses of cash that appear elsewhere – capital spending, changes in working capital, deferred revenue. Free cash flow captures these, but requires turning to another page of the financial report and is hard to forecast as it depends on the timing of payments. But in telecoms where capex is massive, in retail where inventories oscillate, or in software where revenue recognition is key, ebitda misses too much. (more…)

The Advantages of EBITDA

Although there is no silver bullet metric in financial statement analysis, nevertheless there are numerous benefits to using EBITDA. Here are a few:

The Disadvantages of EBITDA (more…)

“We’ll (Berkshire Hathaway [BRK.A][BRK.B]) never buy a company when the managers talk about EBITDA. There are more frauds talking about EBITDA. That term has never appeared in the annual reports of companies like Walmart (WMT), General Electric (GE) or Microsoft(MSFT). The fraudsters are trying to con you or they’re trying to con themselves. Interest and taxes are real expenses. Depreciation is the worst kind of expense: You buy an asset first and then pay a deduction, and you don’t get the tax benefit until you start making money. We have found that many of the crooks look like crooks. They are usually people that tell you things that are too good to be true. They have a smell about them.”