“Central banks have made a $6t commitment to prop up financial markets via asset purchases. That might not limit the collapse in EPS, but it might limit the collapse in share prices,” Citi says.

“Central banks have made a $6t commitment to prop up financial markets via asset purchases. That might not limit the collapse in EPS, but it might limit the collapse in share prices,” Citi says.

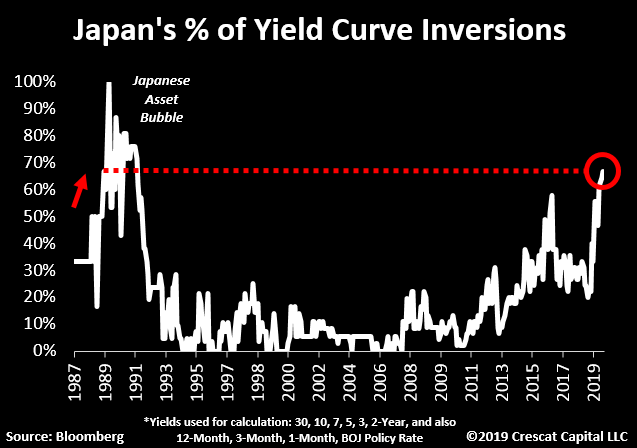

A month prior to the unfolding of its asset bubble crisis.

Credit markets foreshadowing trouble ahead across the globe.

Fitch Ratings on Tuesday forecasted India’s economic growth at 6.6 per cent during the current year, down from 6.8 per cent in the previous year, and said the government has only limited room to ease fiscal policy because of high debt.

It said GDP (gross domestic product) growth is likely to rebound to 7.1 per cent next year.

Keeping India’s rating unchanged at BBB- with a stable outlook, it said the rating balances a strong medium-term growth outlook and relative external resilience with sturdy foreign reserve buffers, against high public debt, financial sector fragilities and some lagging structural factors.

In its Asia-Pacific Sovereign Credit Overview, Fitch said India’s GDP growth decreased for a fifth consecutive quarter in the April-June quarter to 5 per cent, the lowest in six years.

“Domestic demand is faltering, with both private consumption and investment proving lackluster, while the global trade environment is also weak,” it said.

The contribution of gross fixed capital formation (1.3 per cent) remained weak at the same level of the January-March quarter, when it dropped sharply, while the contribution of private consumption fell to 1.8 per cent in the April-June from an average of 4.6 per cent in the preceding four quarters.

Manufacturing grew by only 0.6 per cent, it said.

The government’s policy measures to stimulate the economy include support for the automobile sector, a reduction in capital gains tax, and additional liquidity support for “shadow” banks. Accompanying structural reforms include a further easing of the foreign direct investment (FDI) regime and consolidation of the public banking sector. (more…)

Last two times coincided with the peak of the tech & housing bubble.

Fed policy turning uber dovish with stocks already at record valuations & late in the business cycle? Never ends well.

Most Americans have spent the last few years pressed up against the proverbial bakery window, watching the 1% enjoy a life of ever-increasing wealth and seemingly total indifference to the multitudes who aren’t favored by zero interest rates, big trust funds and political/corporate connections.

The one consolation for the have-nots has been that, by owning few stocks and bonds, they would suffer less when those bubble markets did what bubbles always do, which is burst.

Friday was a small but satisfying taste of that eventuality.

From Bloomberg:

World’s Richest People Lose $68.5 Billion in Stock Selloff

The fortunes of the world’s 500-richest people dropped by $73.9 billion Friday as equity markets swooned with investor worries about the pace of interest rate hikes in the U.S. Warren Buffett led the declines, shedding $3.3 billion to end the day at No. 3 on the Bloomberg Billionaire Index with $90.1 billion.

The chart shows about $100 billion of play money evaporating in the past week. Not enough to seriously inconvenience most of the people on Bloomberg’s billionaires list, but still a nice reversal of fortune versus the average person with a house, small bank account and not much more – who didn’t lose a thing.

As for whether Friday was just a blip in an ongoing “secular bull market” or a sign that fundamentals are at last gaining the upper hand on “liquidity,” that remains to be seen. Longer-term though, there can’t be much doubt that today’s stock and bond valuations are higher than they’ll be during the next downturn.

Here’s a chart from John Hussman’s latest (Measuring the Bubble) that illustrates the point.

If you have been waiting for the “global economic crisis” to begin, just open up your eyes and look around. I know that most Americans tend to ignore what happens in the rest of the world because they consider it to be “irrelevant” to their daily lives, but the truth is that the massive economic problems that are currently sweeping across Europe, Asia and South America are going to be affecting all of us here in the U.S. very soon. Sadly, most of the big news organizations in this country seem to be more concerned about the fate of Justin Bieber’s wax statue in Times Square than about the horrible financial nightmare that is gripping emerging markets all over the planet. After a brief period of relative calm, we are beginning to see signs of global financial instability that are unlike anything that we have witnessed since the financial crisis of 2008. As you will see below, the problems are not just isolated to a few countries. This is truly a global phenomenon.

Over the past few years, the Federal Reserve and other global central banks have inflated an unprecedented financial bubble with their reckless money printing. Much of this “hot money” poured into emerging markets all over the world. But now that the Federal Reserve has begun “tapering” quantitative easing, investors are taking this as a sign that the party is ending. Money is being pulled out of emerging markets all over the globe at a staggering pace and this is creating a tremendous amount of financial instability. In addition, the economic problems that have been steadily growing over the past few years in established economies throughout Europe and Asia just continue to escalate. The following are 20 signs that the global economic crisis is starting to catch fire…

#1 The unemployment rate in Greece has hit a brand new record high of 28 percent. (more…)

In the latest sign yet that things in the world are roughly 25% worse than expected (give or take), the FT reports that the IMF will seek an imminent rise in its lending cap from $750 billion to $1 trillion to build safety nets that could prevent financial crises. “Even when not in a time of crisis, a big fund, likely to intervene massively, is something that can help prevent crises,” Dominique Strauss-Kahn, the IMF managing director told the Financial Times. “Just because the financing role decreases, doesn’t mean we don’t need to have huge firepower … a $1,000bn fund is a correct forecast.” At this point it is glaringly obvious that without the explicit support of the various central banks and of such fake international but really US organizations as the IMF, the already prevalent liquidity crisis would simply destroy the world. The troubling theme is that instead of taking away incremental worries, we have now gotten to the point where one bailout, like a butterfly in China, merely requires 10 more down the road. Alas, instead of a virtuous Keynesian dynamic, this is anything but.

In the latest sign yet that things in the world are roughly 25% worse than expected (give or take), the FT reports that the IMF will seek an imminent rise in its lending cap from $750 billion to $1 trillion to build safety nets that could prevent financial crises. “Even when not in a time of crisis, a big fund, likely to intervene massively, is something that can help prevent crises,” Dominique Strauss-Kahn, the IMF managing director told the Financial Times. “Just because the financing role decreases, doesn’t mean we don’t need to have huge firepower … a $1,000bn fund is a correct forecast.” At this point it is glaringly obvious that without the explicit support of the various central banks and of such fake international but really US organizations as the IMF, the already prevalent liquidity crisis would simply destroy the world. The troubling theme is that instead of taking away incremental worries, we have now gotten to the point where one bailout, like a butterfly in China, merely requires 10 more down the road. Alas, instead of a virtuous Keynesian dynamic, this is anything but.

Some more on the IMF’s feeble attempt at justifying the need for its exploding funding requirements, as well as its own attempt to validate that all is well:

South Korea, as this year’s president of the Group of 20 leading economies, is helping craft the plan. Seoul hopes to convince the G20 countries to back the increased IMF funding at a summit in South Korea in November. The G20 meeting in London in 2009 tripled IMF resources from $250bn. A US official said Washington was sympathetic to improved safety nets but needed more details on the Korean-IMF plan.

South Korean economists forged the plan because of their own bitter experience of their currency and stock market plunging in 2008. In spite of robust economic fundamentals, Seoul needed to be rescued from a dangerous liquidity shortfall by swaps from the US, Japan and China. (more…)

Feb. 24 (Bloomberg) — Ballooning debt is likely to force several countries to default and the U.S. to cut spending, according to Harvard University Professor Kenneth Rogoff, who in 2008 predicted the failure of big American banks.

Following banking crises, “we usually see a bunch of sovereign defaults, say in a few years,” Rogoff, a former chief economist at the International Monetary Fund, said at a forum in Tokyo yesterday. “I predict we will again.”

The U.S. is likely to tighten monetary policy before cutting government spending, sending “shockwaves” through financial markets, Rogoff said in an interview after the speech. Fiscal policy won’t be curbed until soaring bond yields trigger “very painful” tax increases and spending cuts, he said.

Global scrutiny of sovereign debt has risen after budget shortfalls of countries including Greece swelled in the wake of the worst global financial meltdown since the 1930s. The U.S. is facing an unprecedented $1.6 trillion budget deficit in the year ending Sept. 30, the government has forecast.

“Most countries have reached a point where it would be much wiser to phase out fiscal stimulus,” said Rogoff, who co- wrote a history of financial crises published in 2009. It would be better “to keep monetary policy soft and start gradually tightening fiscal policy even if it meant some inflation.”

1. Find and trade markets where your edge is the greatest.

2. Avoid markets were the probability of rule changes and lack of transparency is present.

3. Think of and imagine market scenarios others fail to.

4. Fundamental macroeconomic forces will ultimately prevail.

5. Trading time frames and profit objectives though must coincide with what the market is giving you at any one time.

6. Quantify risk with a multidimensional perspective, not just by one or two measures such as VAR or a price stop.

7. Learn from history. Jay Gould and his attempts to corner the gold markets in the late 1860’s. The Russian default of 1917 and 1998. The European Rate Mechanism break up. The Tequila crisis of 1994. The Asian financial crisis.

8. Be deadly serious, as Gichin Funakoshi said “You must be deadly serious in training”. If you have a position make it a meaningful size and monitor it carefully. I recall many comments from fellow traders the past few years saying something like “I am long EuroSwiss just to have some on but not really watching it.”

9. Define and use a trading methodology that incorporates a process and framework that works for you. Inclusive in this should be a daily routine that includes diet, exercise, family time, etc.

10. Seek out catalysts for CHANGE in markets. Where are the forces, in a Newtonian like law of motion, building up the greatest to cause a CHANGE and movement in markets?