The V-shaped recovery in corporate earnings is complete… With 95% of companies reported, S&P 500 earnings hit a new all-time high in Q1, blowing past the prior high from Q3 2018.

The German DAX is closing up about 1% and in doing so is closing at a new all-time high. The France’s CAC is also closing higher and at the highest level since August 2000. Below is a look at the daily chart of the German Dax.

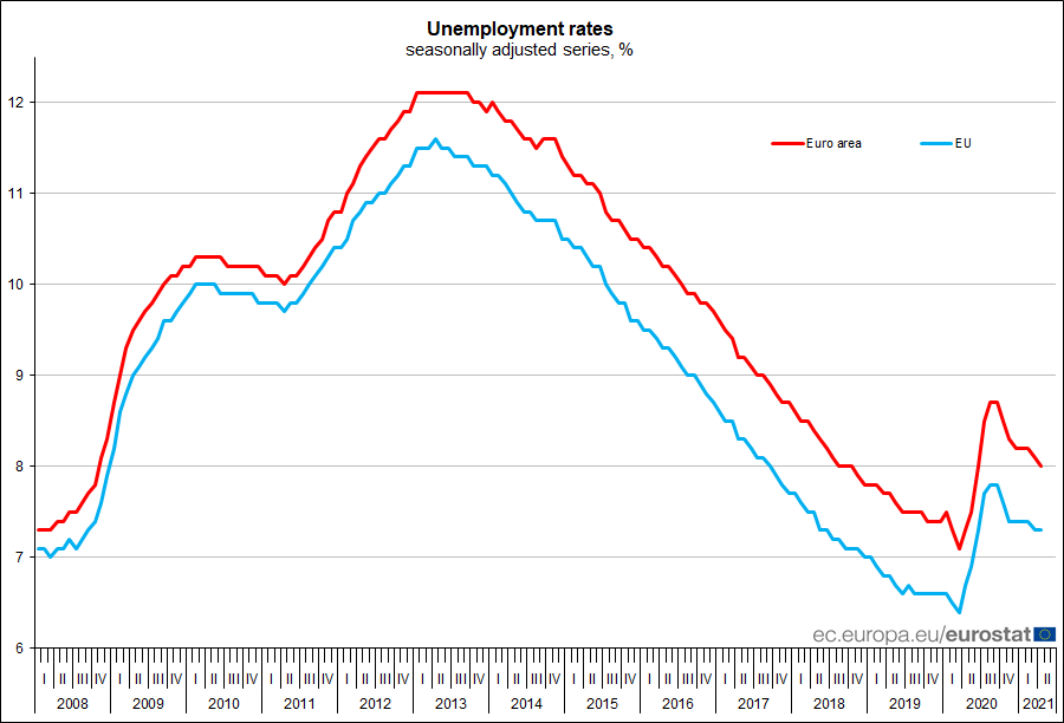

A slight tick lower in the jobless rate but considering the furlough programs in the region, it is tough to draw much conclusions from the reading above.

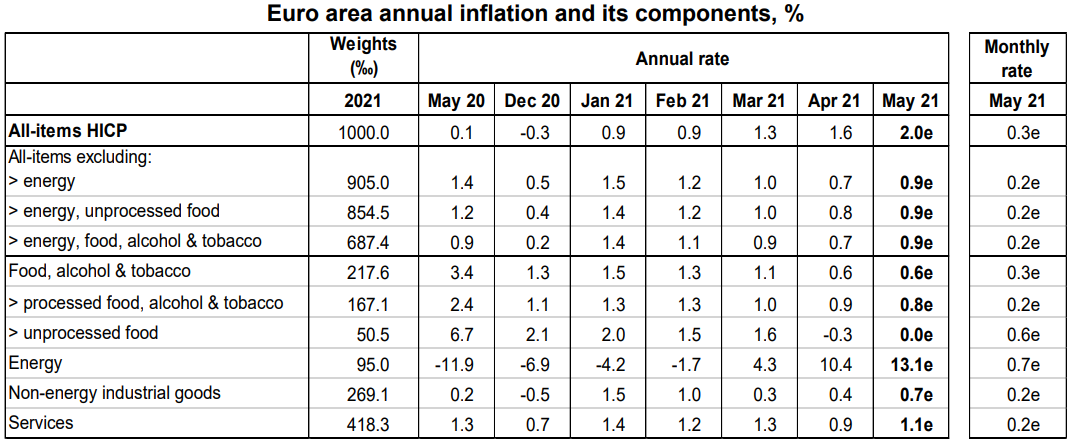

The headline reading is the highest since November 2018 as it reaffirms stronger inflation pressures, which could owe to some part in base effects and also higher input cost inflation across the region/globe.

Oil is searching for a break to the topside as price now extends to its highest since October 2018 with buyers pushing price action above $68 at the moment.

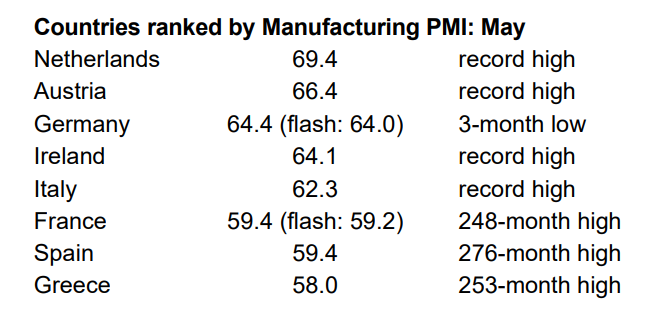

“Eurozone manufacturing continues to grow at a rate unprecedented in almost 24 years of survey history, the PMI breaking new records for a third month in a row. Surging output growth adds to signs that the economy is rebounding strongly in the second quarter.

“However, May also saw record supply delays, which are constraining output growth and leaving firms unable to meet demand to a degree not previously witnessed by the survey.

“High sales volumes are consequently depleting warehouse stocks and backlogs of uncompleted work have soared at a record pace. While these forward-looking indicators bode well for production and employment gains to persist into coming months as firms seek to catch up with demand, the flip-side is higher prices. The combination of strong demand and deteriorating supply is pushing up prices to a degree unparalleled over the past 24 years.

“The survey data therefore indicate that the economy looks set for strong growth over the summer but will likely also see a sharp rise in inflation. However, we expect price pressures to moderate as the disruptive effects of the pandemic ease further in coming months and global supply chains improve. We should also see demand shift from goods to services as economies continue to reopen, taking some pressure off prices but helping to sustain a solid pace of economic recovery.”