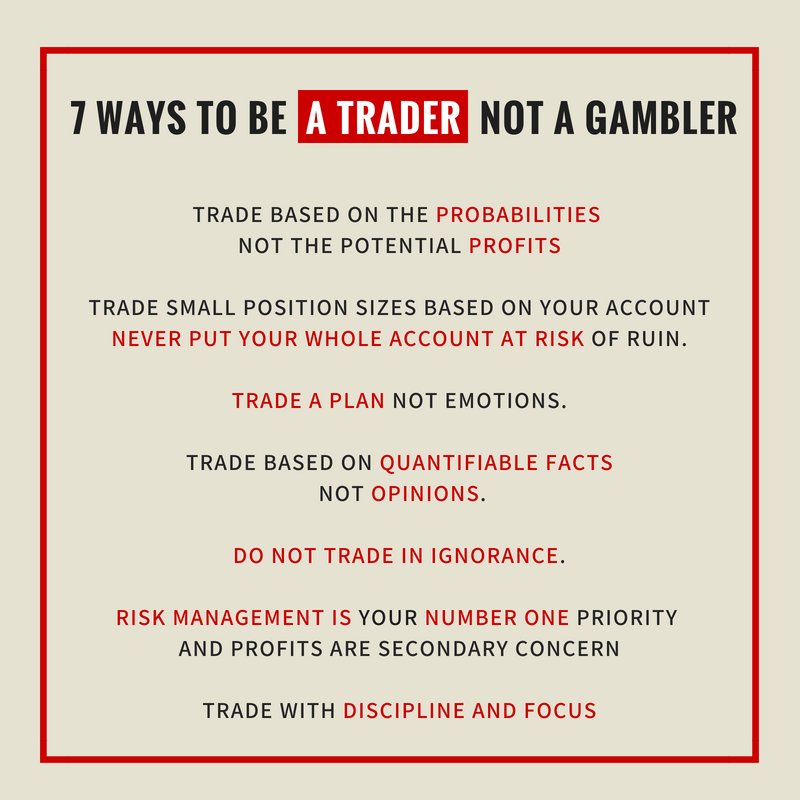

7 Ways to be A TRADER not A GAMBLER

Large All Industry Capex 9.6%

Large Manufacturing Outlook 13 for September

USD/JPY has ticked a little higher in early Asia trade but the response to the release of the BOJ’s Tankan is barely discernible.

The major European indices arre ending the session lower on the day. The provisional closes are showing:

USDJPY: The USDJPY is up testing the topside trend line on the hourly chart. The high for the week at 110.978 would be the next target on a break to the upside. Earlier the price moved above the 200 and then 100 hour MAs (green and blue lines) as buyers retook control from a bearish tilt earlier in the day (below the MAs). (more…)