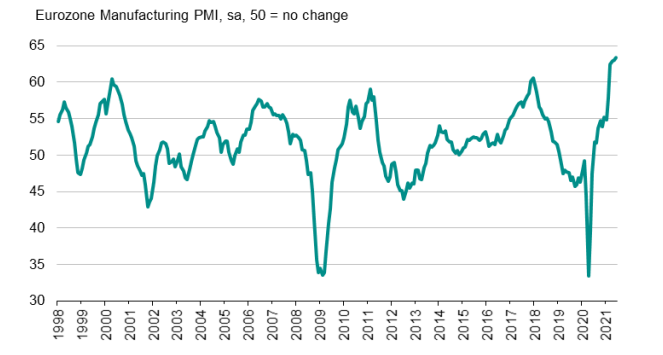

Euro area manufacturing PMI data in focus

The dollar was a solid performer going into the month/quarter-end yesterday with there being not much unwinding even after the London fix.

That takes the likes of EUR/USD back to the post-FOMC lows around 1.1850 and while ranges are narrow today, technicals may come into more importance later before we get to the US non-farm payrolls release tomorrow.

USD/JPY also managed a close above 111.00 and that may prove to be an important technical breakout for the next upside leg to extend.

Data releases won’t offer much in Europe later today as the OPEC+ meeting takes center stage, so focus on the charts instead before the payrolls on Friday.

0600 GMT – Germany May retail sales data

Prior release can be found here. German retail sales is estimated to show a solid bounce in May after a more dismal Q1, with looser restrictions also set to bolster the outlook further going into the latter stages of Q2 and 2H 2021.

0630 GMT – Switzerland June CPI figures

Prior release can be found here. Swiss inflation is expected to keep more subdued despite price pressures in general being more solid across the globe as of late. That will keep things as it is when it comes to the SNB so no change to the narrative there.

0715 GMT – Spain June manufacturing PMI

0730 GMT – Switzerland June manufacturing PMI

0745 GMT – Italy June manufacturing PMI

0750 GMT – France June final manufacturing PMI

0755 GMT – Germany June final manufacturing PMI

0800 GMT – Eurozone June final manufacturing PMI

Focus will be on the final readings in France, Germany, and overall Eurozone though they should not tell us much of anything new since these will be the final releases.

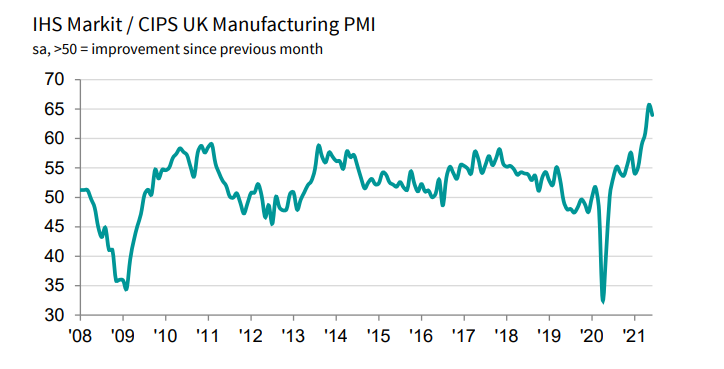

0830 GMT – UK June final manufacturing PMI

The preliminary report can be found here. There shouldn’t be much to add with UK manufacturing conditions keeping more solid after the reopening in April.

0900 GMT – Eurozone May unemployment rate

Prior release can be found here. Labour market conditions in the region are expected to keep steadier and the German report for June does provide some encouragement that things are on the right track going into 2H 2021.

1130 GMT – US June Challenger layoffs, job cuts

Prior release can be found here. A reminder that it is NFP week in the market. The data provides information on the number of announced corporate layoffs by industry and region and acts as a general labour market indicator.