Thought For A Day

Bank of America Global Research outlines 8 reasons for maintaining a bullish bias on USD/JPY into year-end.

“1. JPY’s cyclical bottom has depreciated over time

2. Economic recovery is negative for JPY

3. Commodity bull market

4. Inflation = higher US real yield vs lower JP real yield

5. JPY’s weakness hasn’t been excessive vs other markets

6. Outward FDI could accelerate in 2H21

7. Positioning is not stretched JPY short positioning is not stretched.

8. Chart technical is bearish JPY,” BofA note.

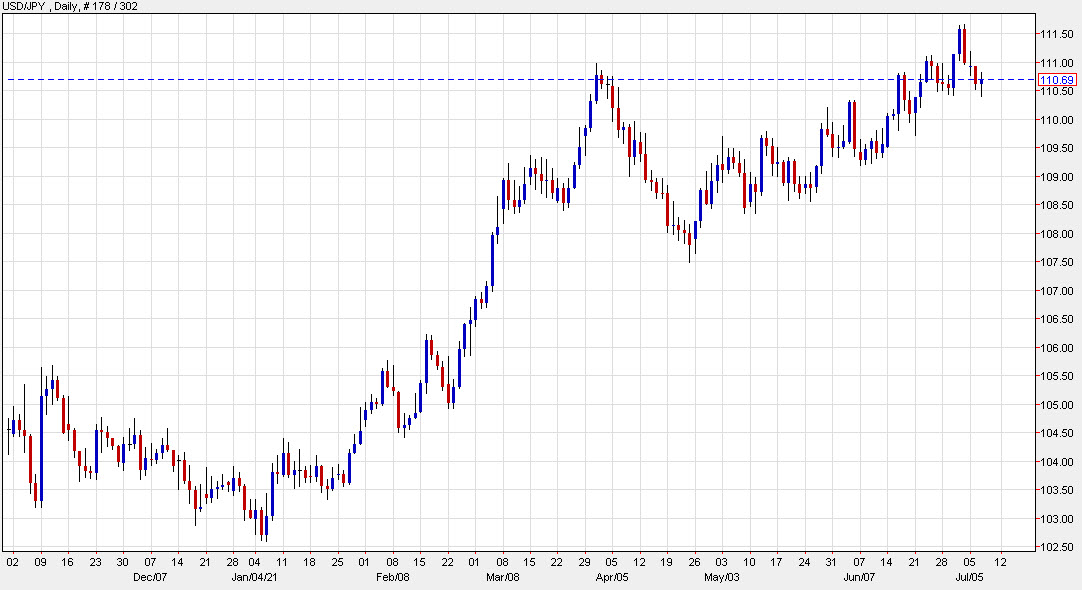

“We estimate USD/JPY’s upside targets at 112.20, the 114s and possibly 115.86. Late-2016/early-2017 highs in the 118s can’t be ruled out,” BofA adds.

For bank trade ideas, check out eFX Plus.

Just be wary that when China issues such statements, they are usually to preempt the market that there might be possible decisions on said matter on the way.