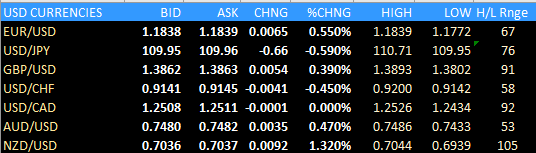

USD/JPY down 0.2% at 109.75

With Treasury yields keeping lower on the day, it is seeing the yen hold firmer ground so far in European morning trade as USD/JPY keeps below 110.00.

The low today hit 109.72 and that nears a test of daily support from the 21 June low @ 109.71. That will be a key level to watch ahead of the close before the 50.0 retracement level @ 109.57 comes into play again – as we saw last week.

There hasn’t been a coherent theme in the market in trading this week with equities and bond yields bouncing higher earlier only to see a retreat over the past day or so.

In particular, 10-year yields have come off the high around 1.42% on Tuesday to fall just below 1.32% currently in European morning trade today.

Going back to USD/JPY, as price action continues to tussle around this area, the 100-day moving average (red line) – now seen @ 109.35 – will also draw closer and may play a key technical role in dictating which direction the pair moves next.

Tomorrow’s US retail sales data may be a catalyst for a move so just be wary of that.