CFTC positioning data

One of the big theories on the drop in Treasury yields in the past month or so is that it was a big squeeze on shorts.

If so, it might be over.

The just-released CFTC data shows that 10-year futures positioning is now a net long of 55,987 contracts compared to a net short of 25,593 a week ago. The data are for the close on Tuesday though, and yields have continued to fall since then.

Outside of 10s, futures market specs remain short with barely anyone covering a good-sized short in 30s. There was some short covering in 2s and 5s by around 20% of the positions.

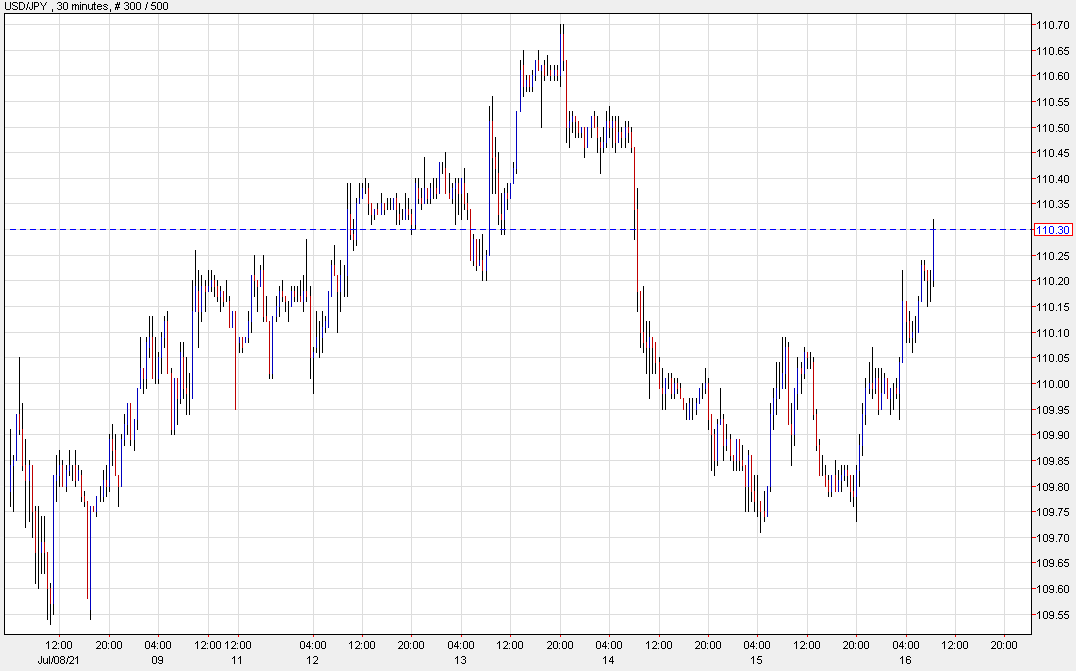

10-year yields: