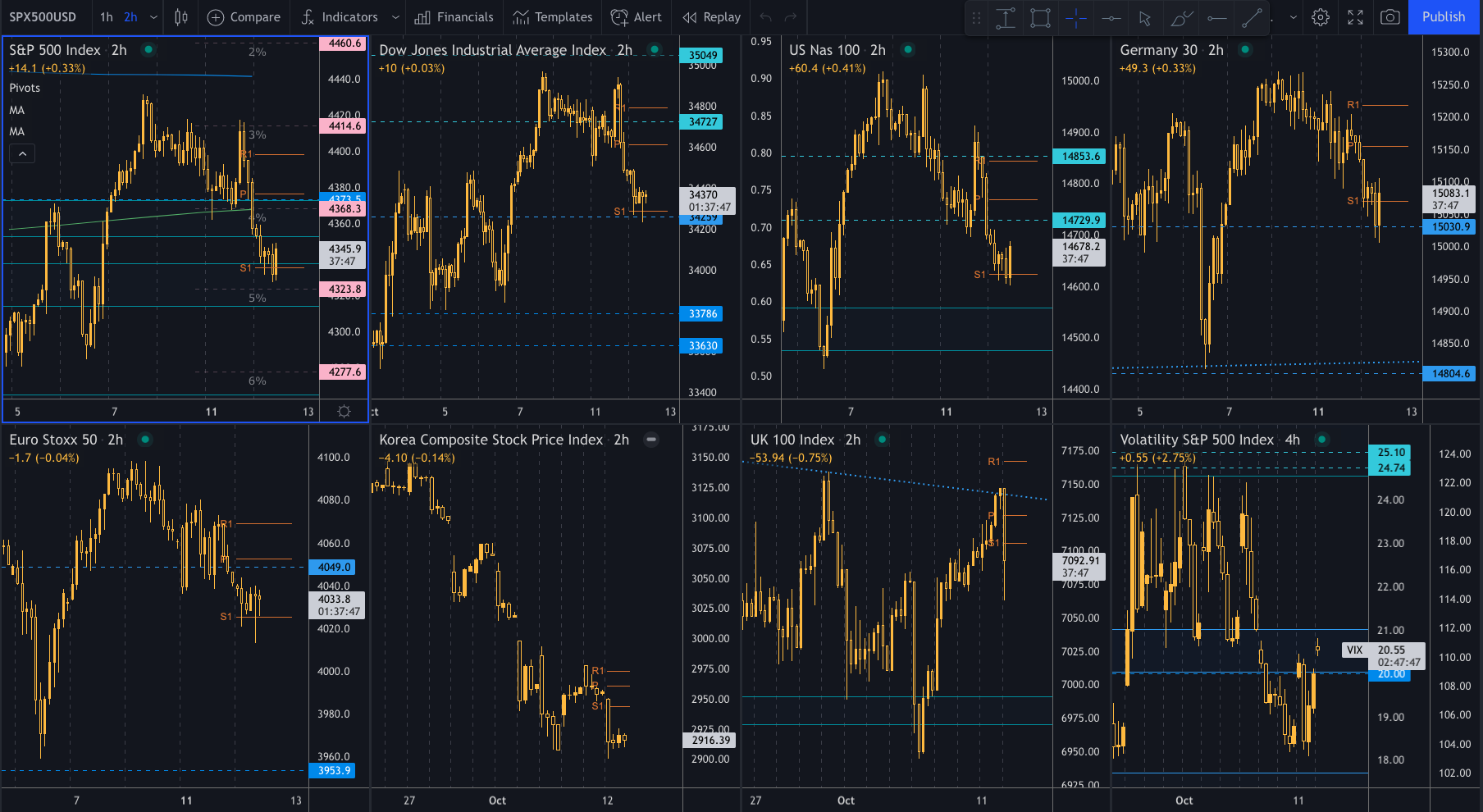

Stocks struggle to move higher

The US stocks could not sustain positive levels and drifted lower into US afternoon. The major indices are closing lower for the third consecutive day.

At the close, Apple announced that they would have to cut production of the iPhone due to chip crunch. Apple shares are down -1.1% after the close.

- Dow S&P and NASDAQ post a three day stock decline

- S&P closes around 4% from its all-time high

- Dow closes about 3% from its all-time high

- NASDAQ closes -6% below its all-time high

The final numbers are showing:

- Dow Jones -117.72 points or -0.34% at 34378.33

- S&P index -10.56 points or -0.24% at 4350.64

- NASDAQ index -20.27 points or -0.14% at 14465.93