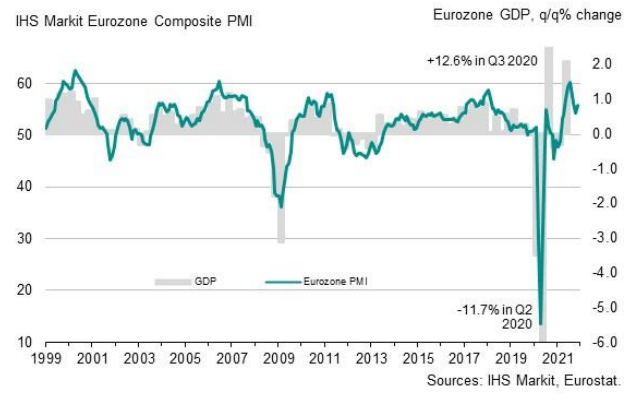

The PMI beats in France and Germany today come with some caveats

While services and manufacturing output saw an improvement in November, it comes after a period of sluggishness over the past four months and there are little signs that this latest bounce is going to be a meaningful or lasting one.

For one, the boost to services activity may already be stale by the end of the month already (data collected from the PMI readings are up until 19 November) considering that virus restrictions are starting to come back into the picture.

On that front, France is perhaps less impacted than Germany, so I’d take the improvements this month with a pinch of salt until there is evidence that the virus situation in Germany isn’t going to lead to limitations on business activity in the weeks ahead.

Besides that, supply and capacity constraints are still ever persistent and ongoing across the region. That is weighing on overall business sentiment while also keeping input and output costs elevated.

Eventually, the latter will feed into higher inflation pressures and in turn perhaps weigh on client and domestic demand in general.

So, while the readings are good on paper today, that is merely what it has to offer. The details reveal that there are troubling times perhaps just around the corner for Europe.