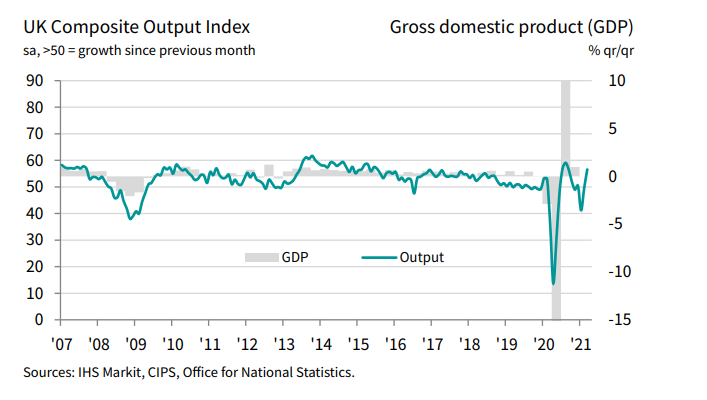

Latest data released by Markit/CIPS – 24 march 2021

- Prior 49.5

- Manufacturing PMI 57.9 vs 55.0 expected

- Prior 55.1

- Composite PMI 56.6 vs 51.4 expected

- Prior 49.6

That is a solid beat and adds to the optimism surrounding the rebound in the UK economy once restrictions are eased later on in the year.

Business activity in the UK returned to expansion and improved at its quickest pace in seven months, with the services reading also coming in at the highest since August last year. Meanwhile, the manufacturing reading is the highest in 40 months.

Service providers noted forward bookings from domestic consumers as the higher level of activity is linked to the prospect of looser restrictions later in the year.

Manufacturers also noted advanced orders helping to boost demand conditions as export sales remain relatively subdued. Markit notes that:

“The UK economy rebounded from two months of decline in March, with business activity growing at its fastest rate since last August as children returned to schools, businesses prepared for the reopening of the economy and the vaccine roll-out boosted confidence. Companies reported an influx of new orders on a scale exceeded only once in almost four years, and business expectations for growth in the year ahead surged to the highest since comparable data were first available in 2012. Employment consequently rose for the first time since the pandemic struck as firms expanded capacity in response to the new inflows of work and brighter outlook.

“The surge in business activity is far stronger than any economists expected, according to Reuters polls, and hints at only a modest contraction of GDP during the first quarter, adding to evidence that the economy has shown far greater resilience in the third lockdown compared to the first. The encouraging readings on future expectations, job creation and new order inflows meanwhile all point to robust economic growth in the second quarter, especially if virus restrictions are lifted further.

“Worries persist though, especially in relation to near-record supply chain delays, a continued fall in exports and sharply rising prices, all of which are making life difficult for many companies. Many consumer facing companies meanwhile remain constrained by COVID-19 restrictions, which are likely to curb the overall pace of economic growth for some time to come, especially if we see a third wave of infections.”