Combined net worth: $1 trillion.

the major European indices end the day mostly higher. The exception is the German Dax which fell marginally. The Italian FTSE MIB is also a little lower.

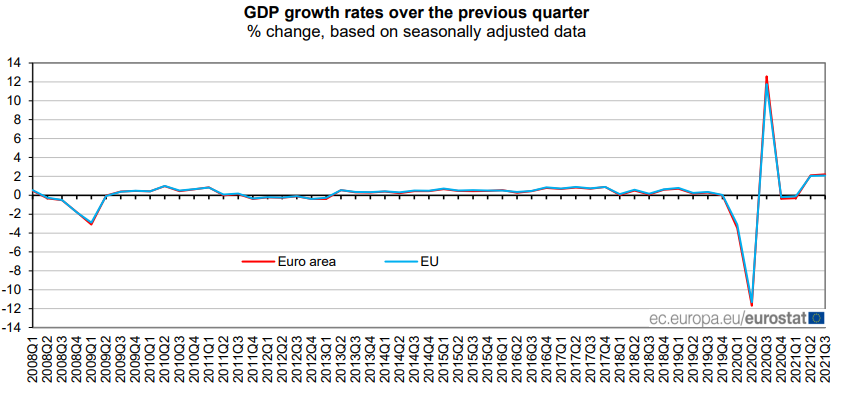

The euro area economy grew by a little more than expected as overall conditions picked up further after the easing of restrictions that began in Q2. The outlook is still a worry though considering rising inflation and supply bottlenecks persisting.

The hawkish tilt was in the headlines. QE has ended and rate hikes are now expected sometime in the middle quarters of 2022. Prior to the meeting the expectations were for the BoC to reduce QE from CAD$2 billion per week to CAD1$ billion per week and interest rate hikes were not expected until the second half of 2022.

GDP revised lower

The 2021 GDP figure is now revised lower to 5.1% from 5.0^% expected and 6.0% previous. However, 2022 and 2023 growth was both revised higher

Inflation concerns

Like most central banks the BoC expressed its concern for rising inflation. The BoC is now ‘closely watching inflation expectations and labour costs to ensure that the temporary forces pushing up prices do not become embedded in ongoing inflation’. The causes for the inflation by the BoC is seen as increased demand for goods, but shortage in labour and production & distribution alongside surging energy prices.

The output gap

The output gap is the difference between GDP and the potential GDP. It gives you a snapshot of how the economy is performing compared to its possible performance. The current gap is less than it was in Q2 (-3 to -2%) and is now at -2.25 and -1.25%. The gap is expected to close around the middle quarters of 2022.

Summary

It was good news for the CAD out of the meeting and this should result in some CAD strength over the medium term, at least on dips as it could be argued that much of the good news was priced in. If the BoE push back against the strong rate hikes projected by SONIA futures next week (no less than four 25bps hikes projected for 2022) then more GBPCAD downside looks attractive. Be aware this outlook is dependent on the BoE meeting next week as there needs to be a deeper divergence between the BoC and the BoE to initiate a medium term trade.

Bitcoin will be 100% green by 2024. No other system will be more green.