Modest change in the weekly Baker Hughes rig count data

The Baker Hughes rig count data for the current week is showing:

- Oil rigs 342 versus 343 last week

- Gas rigs 96 versus 94 last week

- Total rigs 440 versus 438 last week.

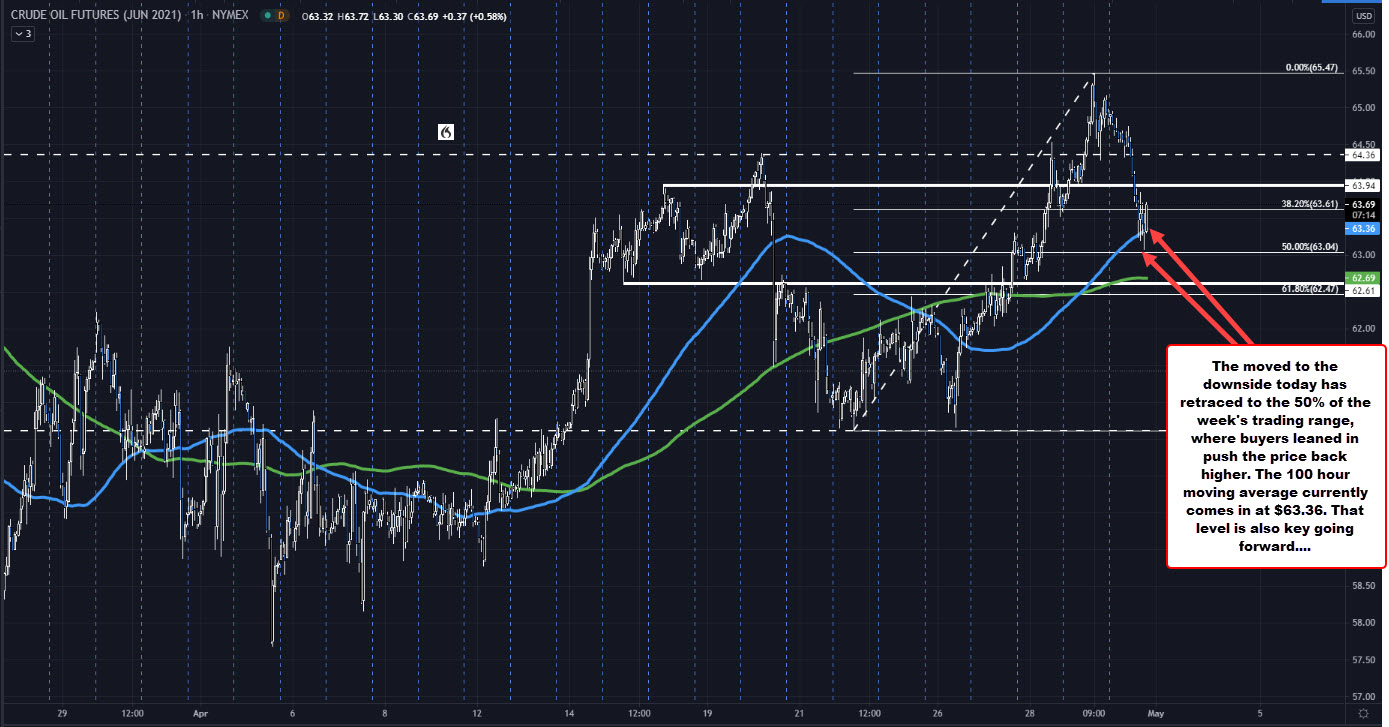

The price of WTI crude oil futures is currently trading down $1.48 or -2.26% $63.55. The high price reached $64.95. The low price is at $63.08.

Looking at the hourly chart, the low price today stalled just ahead of the 50% retracement of the range for the week at $63.04. On the move down, the price did also move below its 100 hour moving average currently at $63.36, but could not sustain the downside momentum.

Going forward, the moving average and 50% retracement remains a key downside support target. If the price can move below each, the bears would increase their control.