Happy Friday

The economic calendar is fairly light today today. The highlight will be new home sales at 10 AM ET. Recall earlier this week the existing home sales which accounts for 90% of the housing market in the US rose to a annualized sales pace of 4.75 million from 3.91 million previously. That was good enough for a 21.4% gain. Supply remains a huge concern in the housing market. For the new sale market, builders reluctant to start new projects as a result of the pandemic. However, they too are rebounding in recent months. The expectation is for a rises to 700 K from 676K last month.

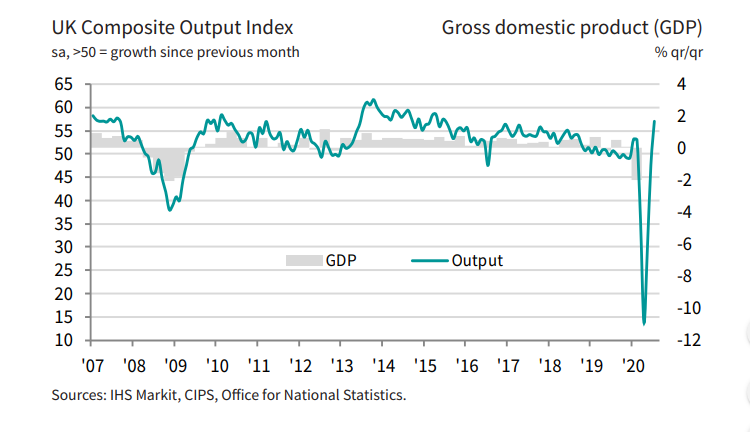

In other economic releases the US market manufacturing index for the month of July (preliminary) will be released at 9:45 AM ET/1345 GMT. The expectation is for a rebound back above the 50.0 level. The expectation is for a rises to 52.0. Last month the index came in at 49.8. The service PMI is also expected to rise to 51.0 from 47.9 last month

The Baker Hughes rig count will be released at 1 PM ET/1700 GMT. The oil rig count is expected to fall to 179 from 180 last week. The total rig count is expected to rise to 255 from 253 last week.

The focus will be on the equity markets. The various headlines from the economic relief package also be of interest.

Investing:

Investing: