A light one on the data docket once again

Good day, everyone! Hope you’re all doing well as we get things going in the session ahead. There hasn’t been much major movement on the day so far but the yen is a little weaker amid higher Treasury yields this time around today.

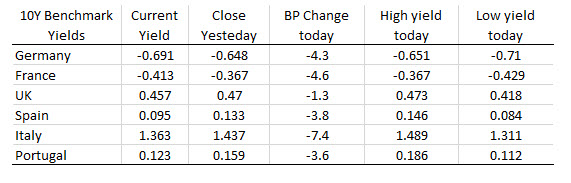

The back and forth action in bonds this week is largely to do with positioning as all eyes are on the Fed and the Jackson Hole symposium later in the week.

Looking ahead, there isn’t much else to shake things up so just be on the look out for trade and Brexit developments. Otherwise, risk sentiment will remain a key factor and as such, keep your eyes on the bond market.

0830 GMT – UK July public sector debt data

Prior release can be found here. A glimpse of the UK budget and public finances but it isn’t a major data point at this point in time.

1100 GMT – US MBA mortgage applications w.e. 16 August

Weekly US housing data, measures the change in number of applications for mortgages backed by the MBA during the week. Not the biggest of data points, but a general indicator of the housing sector sentiment.

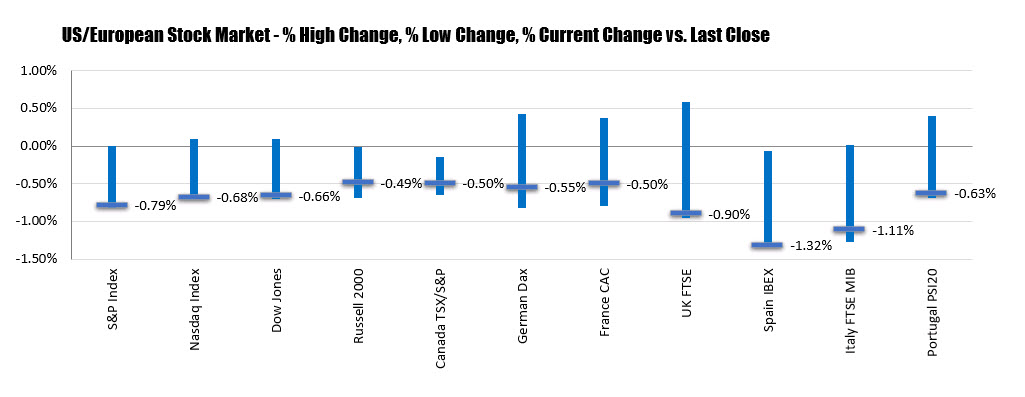

The major indices open lower but did recover midday and traded marginally higher before reversing and moving back down.

The major indices open lower but did recover midday and traded marginally higher before reversing and moving back down.