US and European stocks jumped, government bonds sold off and the pound leapt as investors remained hopeful British and EU negotiators were close to a draft deal on Brexit. The S&P 500 finished 1 per cent higher in New York on Tuesday in a broad-based rally that was the benchmark’s fourth advance in five sessions and left it about 1 per cent from its record high close in late July. Healthcare was the best-performing sector in the index as investors cheered earnings from Johnson & Johnson, while the telecommunications services and technology sectors were next best. Several key banks including JPMorgan, Citigroup, Wells Fargo and Goldman Sachs reported earnings ahead of the open in New York. In early trade, JPMorgan was the standout gainer, but the broad market rally today ultimately lifted the share prices of rivals.

The Nasdaq Composite rose 1.2 per cent. US Treasuries tumbled, driving yields higher. The yield on the benchmark 10-year Treasury was up 1.8 basis points to 1.771 per cent, having been down 4 bps earlier in the session. European stocks extended gains to leave the broad Stoxx 600 up 1.1 per cent and Germany’s Dax up 1.2 per cent. London’s FTSE 100 closed fractionally lower. Sterling was up 1.2 per cent in afternoon trade in New York to $1.2766 and gained 1.3 per cent against the euro to €1.1572, its highest since May, spurred along by a Bloomberg report that UK and EU negotiators were now close to a draft Brexit deal.

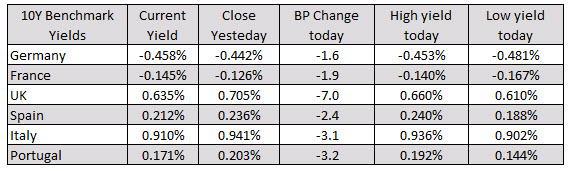

Reflecting the sell-off in the government bond markets, the yield on the UK 10-year Gilt was up 0.6 bps to 0.699 per cent, while that on the Germany’s 10-year Bund rose 1.9bp to minus 0.405 per cent. Earlier in the day, Michel Barnier, Brussels’ chief Brexit negotiator, has said a new withdrawal deal between the EU27 and the UK is “still possible” this week, but warned that it has become “more and more difficult” as the clock ticks towards a crucial bloc summit starting on Thursday. Figures released earlier Tuesday showed investor sentiment about the German economy declined less than expected in October, while remaining subdued over worries about the US-China trade war and the potential for a disruptive Brexit. Asian equity markets were mixed, with Japan’s Topix outperforming as traders returned from a holiday.

China’s CSI 300 gauge of Shanghai- and Shenzhen-listed names fell 0.4 per cent after data showed consumer price inflation increased at its fastest pace in six years in September. US Treasury secretary Steven Mnuchin warned overnight that a new round of tariffs set for December 15 on $156bn of Chinese goods would be triggered if Beijing failed to seal the limited deal tentatively struck with Donald Trump last week, underlining the fragility of that truce. “Not enough was achieved to alter meaningfully the fundamental global economic outlook, in our view,” said Mark Haefele, chief investment officer at UBS Global Wealth Management. “We maintain an underweight to equities. We will be looking for signs of progress on unresolved trade issues and a response in the economic data that might lead us to reassess our positioning.”