But much depends on the US-China trade war still

The bias has turned more favourable in the most recent poll with a slim majority of respondents (53/102) viewing that risks to the outlook are now skewed more to the upside.

In comparison, just three months ago, a clear majority of respondents (69/97) viewed that risks to the outlook were skewed more to the downside instead.

A lot of this of course owes to the more optimistic US-China trade rhetoric, as both countries look to move closer towards a trade truce by the end of this year.

Among those who answered an additional question in the poll, 50 respondents said the bull run in the stock market will end within a year with 40 respondents saying that it would within the next two years.

That shows that sentiment is leaning more towards the bull run still going strong although I reckon its strength may not be as what we are seeing this year.

I mean with stretched valuations, flagging global growth and more political uncertainty i.e. US elections all at play next year, the S&P 500 may find it tough to post another 25% year like this one and so will its peers.

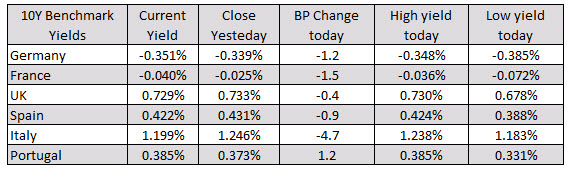

In other markets as European/London traders look to exit:

In other markets as European/London traders look to exit: