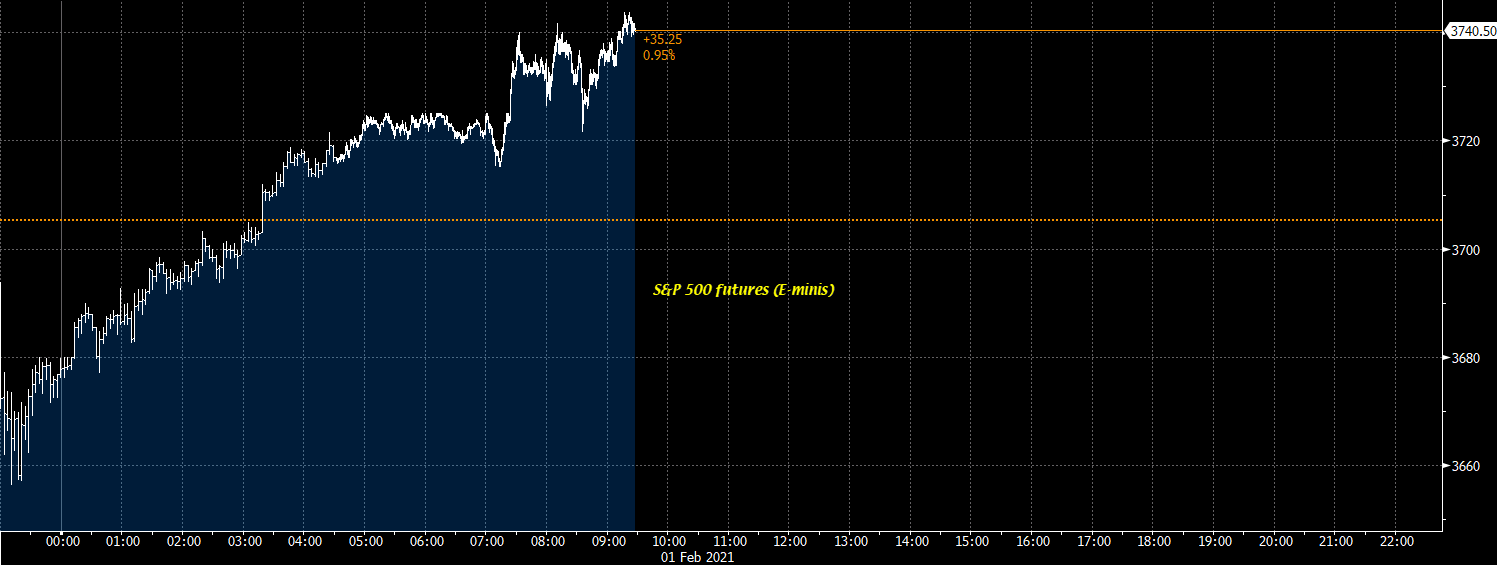

GOP proposal includes $1000

10 US Republicans Senators are out with an alternative proposal to Biden’s $1.9 trillion stimulus. The price tag is $618B and includes:

- $160B for direct pandemic response, $132B for UI

- $20B for child care, $20B for schools

- $50B for small businesses

- $220B for direct payments ($1,000)

- $12B for nutrition

- $4B for mental health service

One thing that isn’t included is $15/h minimum wage, which isn’t a surprise.

If Democrats want a bi-partisan package, this is basically the starting point so you would expect it to go up.

I get the sense that Democrats are planning on using reconciliation anyway and bypassing Republicans but politics is a tough thing to predict. With this though, you can feel secure that more money is coming (and probably headed straight into call options in meme stocks).

More details: