This will come as no surprise, but a catch up on the Phase 1 ‘trade deal’.

This via The Peterson Institute for International Economics (PIIE), an independent nonprofit, nonpartisan research organization:

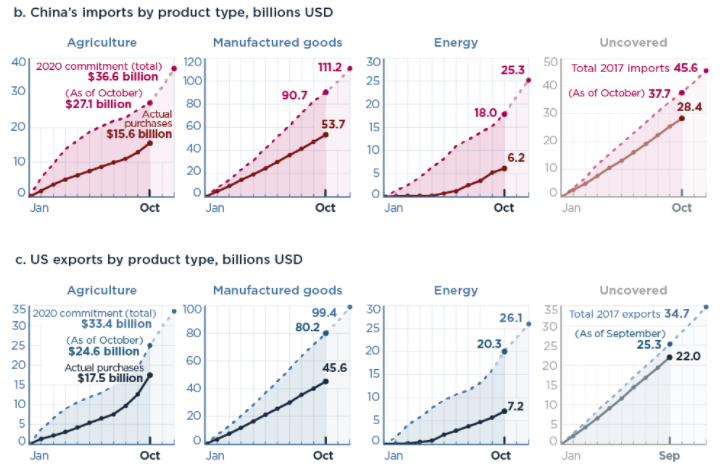

- With ten months of 2020 now in the books, China has purchased less than half of the US exports Trump pledged it would buy this year under his Phase One deal.

There is plenty of detail in the group’s report, here is the link.

In Summary:

There are still 2 months to go on this year’s figures but any non-biased assessment will conclude the actual will fall well short of the promised targets. The pandemic is often cited as a reason for the gap between target and actual.