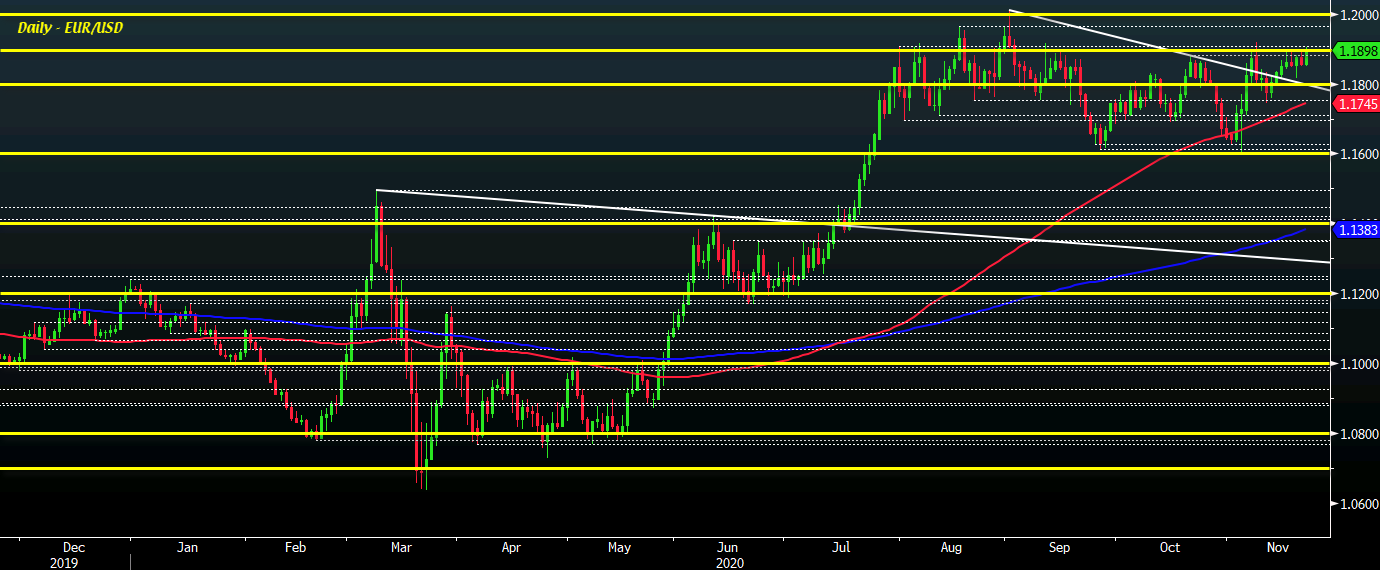

DXY taking out the lows for a year on a closing basis

Wednesday:

Thursday is US Thanksgiving and Friday is also a de facto holiday as well as Black Friday.

President-elect Biden is expected to name some of Cabinet picks on Tuesday,

President-elect Joseph R. Biden Jr.’s transition team will officially announce its first cabinet appointments on Tuesday, said Ron Klain, Mr. Biden’s incoming White House chief of staff, although he declined to say which ones.

The names of at least three expected cabinet appointments were released on Sunday night by people close to the decision process, including Anthony J. Blinken for secretary of state, Jake Sullivan as national security adviser and Linda Thomas-Greenfield as ambassador to the United Nations. – NY Times

I’m hearing rumours we may see an emergency “temporary #Brexit deal” agreed this week to avoid #NoDeal happening in midst of #COVID19.

If this is true, it’s important to point out that this will *not* be a “deal”.

It’s essentially an extension. The problem doesn’t go away.

Otherwise, we are likely to see the can kicked down the road again and I firmly believe that at the end of the day, both sides will fall back on some technicality to sell a compromise.

A skinny deal excluding the three key outstanding issues (instead postponing them) will allow Boris Johnson to “technically” stick with a Brexit on 1 January 2021 while the EU doesn’t have to move its red lines and be made to look worse off from any deal.

“The good old days are over… the cold war hawks in the US have been in a highly mobilised state for several years, and they will not disappear overnight.”

Much like you would expect, Zheng also reaffirmed the continued divide between the US and China in saying that:

“American society is torn apart. I don’t think Biden can do anything about it. He is certainly a very weak president, if he can’t sort out domestic issues, then he will do something on the diplomatic front, do something against China. If we say Trump is not interested in promoting democracy and freedom, Biden is. Trump is not interested in war… but a Democratic president could start wars.”

More:

The Ministry of Trade and Industry has revised their 2020 GDP growth forecast to -6.5% to -6% (previous forecast -7% to -5%)

The forecasts are being bumped up a little as officials see an end in sight for COVID-19 outbreaks.