Gold to S&P 500 just broke out from a bullish pennant. All happening right before next week’s political madness. What a set up.

Reserve Bank of Australia, Governor Phillip Lowe,0.25%, meets 03 November

Going into their latest October meeting some analysts had been anticipating a potential RBA cut. As it turned out the RBA kept rates on hold, but they signalled that they would continue to consider how additional monetary easing could support jobs:

“The Board views addressing the high rate of unemployment as an important national priority. It will maintain highly accommodative policy settings as long as is required and will not increase the cash rate target until progress is being made towards full employment and it is confident that inflation will be sustainably within the 2-3 per cent target band. The Board continues to consider how additional monetary easing could support jobs as the economy opens up further”

You can read the full statement here. This opened up the potential for a rate cut ahead and at the time of writing the OiS markets now price in a 84% chance of a rate cut for November’s meeting. The RBA watcher McCrann also moved to expecting a ‘rate cut’ plus on Cup Day. So, a rate cut I snow the base case for this week.

Of other note is that Australia’s Government announced an aggressive stimulus package on October 06. There is now a large fiscal deficit plan in place to support the country and, according to analysts, there will be few ‘losers’ in stocks. This will help the ASX200 catch up with its Asian peers since a rebound started in March of this year. Australian shares will also be helped by a weaker AUD and as bond yields drift lower towards zero after the Reserve Bank of Australia kept open a rate cut ahead after yesterday’s RBA meeting. SO, stocks have been hit on the latest lockdowns but medium term buyers should be rewarded if they stay the course.

Remember that the Australian economy is closely tied to China’s economy. Approximately 30% of Australia’s GDP comes from its trade with China. Therefore, expect the AUD to be pushed or pulled along with the US-China trade sentiment. If Trump wins the US election then that should drag AUD lower as trade tensions between US and China will ramp up. There is also a very strong correlation between the S&P500 and the value of the AUD. A falling S&P500 tends to weaken the AUD and vice versa, so keep an eye on the latest US stock moves as well in deciding the next path for AUD

Manufacturing 51.4

Non-manufacturing 56.2

Composite 55.3

Official Purchasing Manager’s Index (PMI) from China’s National Bureau of Statistics.

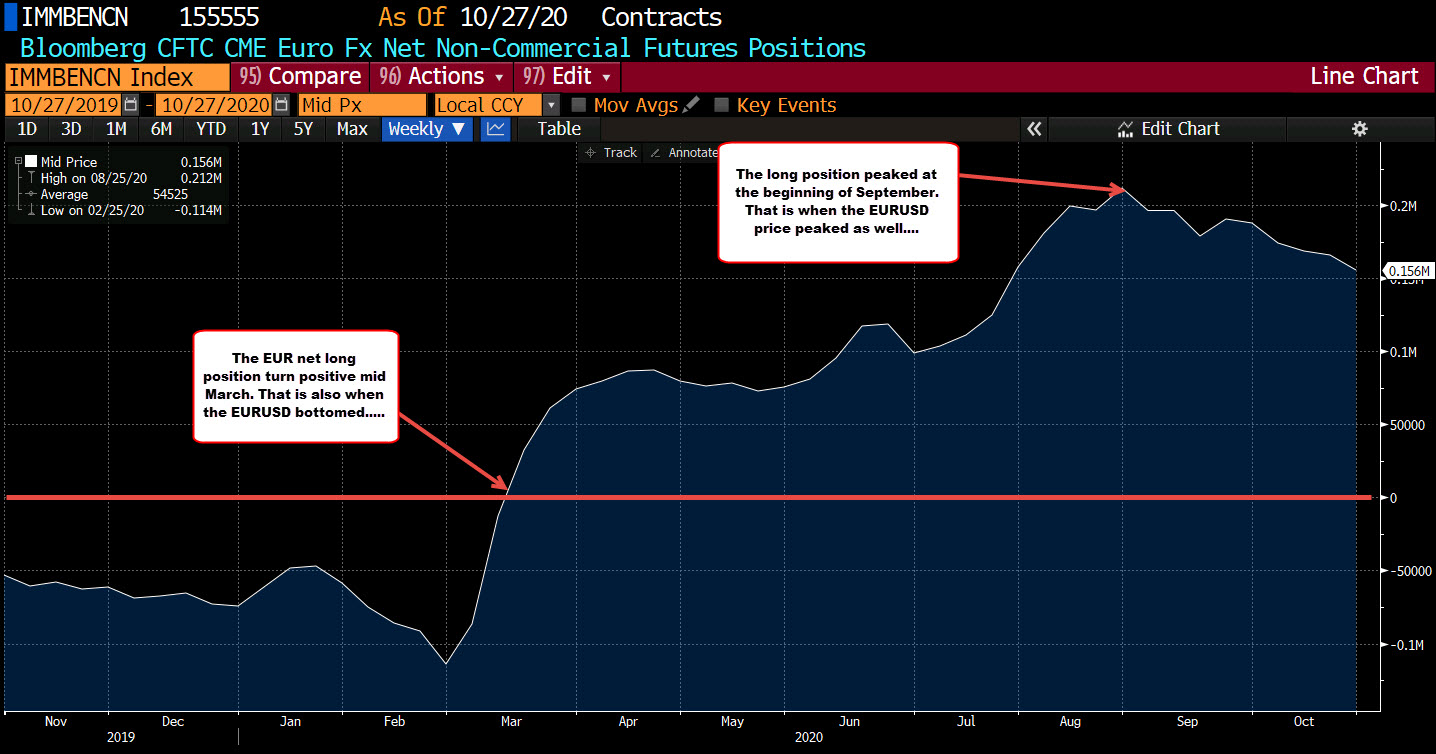

Net positions remained relatively modest with the exception of the long in the EUR. Although still large at 156k, that position is down from a record long level of 212K from the 1st week of September.