The full statement of the 7 July monetary policy decision by the RBA

At its meeting today, the Board decided to maintain the current policy settings, including the targets for the cash rate and the yield on 3-year Australian Government bonds of 25 basis points.

The global economy has experienced a severe downturn as countries seek to contain the coronavirus. Many people have lost their jobs and there has been a sharp rise in unemployment. Leading indicators have generally picked up recently, suggesting the worst of the global economic contraction has now passed. Despite this, the outlook remains uncertain and the recovery is expected to be bumpy and will depend upon containment of the coronavirus. Over the past month, infection rates have declined in many countries, but they are still very high and rising in others.

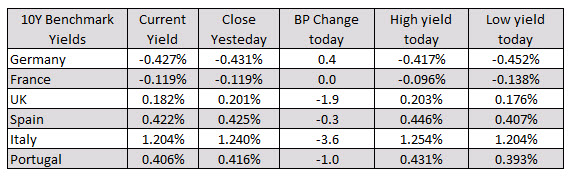

Globally, conditions in financial markets have improved. Volatility has declined and there have been large raisings of both debt and equity. The prices of many assets have risen substantially despite the high level of uncertainty about the economic outlook. Bond yields remain at historically low levels.

In Australia, the government bond markets are operating effectively and the yield on 3-year Australian Government Securities (AGS) is at the target of around 25 basis points. Given these developments, the Bank has not purchased government bonds for some time, with total purchases to date of around $50 billion. The Bank is prepared to scale-up its bond purchases again and will do whatever is necessary to ensure bond markets remain functional and to achieve the yield target for 3-year AGS. The yield target will remain in place until progress is being made towards the goals for full employment and inflation.

The Bank’s market operations are continuing to support a high level of liquidity in the Australian financial system. Authorised deposit-taking institutions are continuing to draw on the Term Funding Facility, with total drawings to date of around $15 billion. Further use of this facility is expected over coming months. (more…)

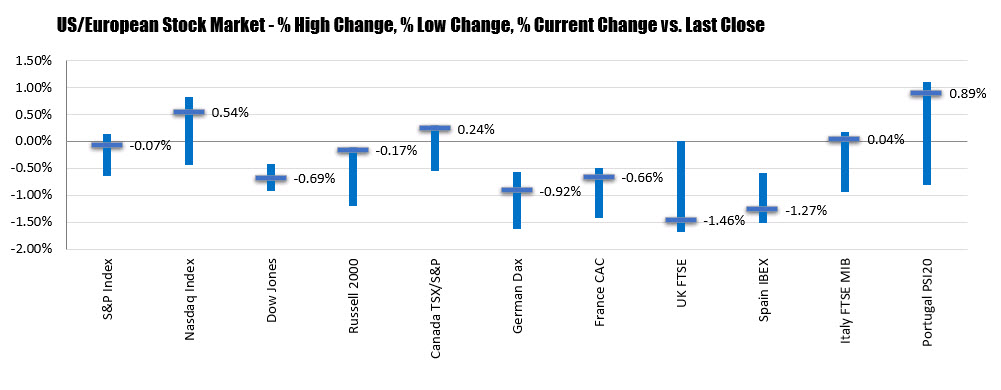

In the US market, the NASDAQ index remains higher. The S&P index did move into the black briefly, but the Dow industrial average remains negative on the day at -0.69%. The S&P index and NASDAQ index are on a 5 day winning streak.

In the US market, the NASDAQ index remains higher. The S&P index did move into the black briefly, but the Dow industrial average remains negative on the day at -0.69%. The S&P index and NASDAQ index are on a 5 day winning streak.