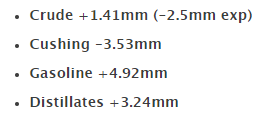

A couple of light data points to move things along

Good day, everyone! Hope you’re all doing well as we look to get things going in the session ahead. Markets are still keeping steady for the most part as we continue to count down to the big risk events yet to come later on in the week.

There has been plenty of hoo-ha since overnight trading over the USMCA deal but I would expect any market reaction on an official announcement to be modest given how this has been in the works for quite some time already now.

Looking ahead, there isn’t much else to shift the dial in markets as we continue to look towards key central bank meetings, the UK election and US-China trade news.

0745 GMT – France October industrial, manufacturing production data

Prior release can be found here. General indication of French factory activity to start Q4. Not a major release by any means.

0930 GMT – UK October monthly GDP data

0930 GMT – UK October manufacturing, industrial, construction output

Prior release can be found here. All the focus remains on the UK election for the pound so the data here will have minimal impact. In any case, it should just reaffirm flat/sluggish economic conditions in the UK to start the final quarter of the year.

0930 GMT – UK October trade balance data

Prior report can be found here. A general indication of trade conditions in the UK economy. A minor data point.

1000 GMT – Germany December ZEW survey current conditions, expectations

Prior release can be found here. Economic sentiment is expected to improve – in-line with other survey data – as the outlook for the German economy is seen to be less gloomy. That said, any signs of a solid recovery is still far away and there are still plenty of challenges that remain as we look towards next year. For now, hope springs eternal.

1100 GMT – US November NFIB small business optimism index

Prior release can be found here. This is an index which measures the opinion of small businesses on the economic conditions in the country. A minor data point.

That’s all for the session ahead. I wish you all the best of days to come and good luck with your trading!