US-China ‘phase one’ talks are getting more complicated and could slide into next year, according to a breaking Reuters report that cites ‘people close to the White House’.

The problem is that top US trade officials fear that rolling back tariffs in a deal that doesn’t address IP and tech transfer issues would not be seen as a ‘win’ for the President.

Negotiations also are complicated by conflicts within the White House about the best approach to China, and by the fact that Trump could veto any agreed deal at the last minute.

The report is weighing on risk trades.

A short time ago, Bloomberg was a out with a report saying that talks are at a sensitive stage and could easily fall apart but that they’re ‘making progress in key areas’.

That report gave a small lift to USD/JPY.

The contents of the story weren’t particularly upbeat and didn’t advance the story much but the headline was: ‘Trump’s China Trade Deal Edges Ahead as Risk of Collapse Looms’, and the market ran with the positive take.

That story highlights how the deteriorating situation in Hong Kong and the bill that will require sanctions on any country that undermines its special status.

It also said that in the recent deputy-level meeting, they agreed to accelerate talks in order to avoid new tariffs. They also made progress on IP and enforcement but failed to make headway on agricultural purposes.

In other markets as European/London traders look to exit:

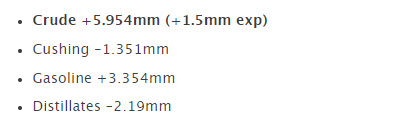

In other markets as European/London traders look to exit: The price of crude oil has moved higher after the lower than expected build. The price currently trades at the high for the day at $56.12. The lower earlier in the day extended down to $55.16.

The price of crude oil has moved higher after the lower than expected build. The price currently trades at the high for the day at $56.12. The lower earlier in the day extended down to $55.16.