Trump says economy doing well

Trump tweet:

Our Economy is very strong, despite the horrendous lack of vision by Jay Powell and the Fed, but the Democrats are trying to “will” the Economy to be bad for purposes of the 2020 Election. Very Selfish! Our dollar is so strong that it is sadly hurting other parts of the world. The Fed Rate, over a fairly short period of time, should be reduced by at least 100 basis points, with perhaps some quantitative easing as well. If that happened, our Economy would be even better, and the World Economy would be greatly and quickly enhanced-good for everyone!

Nothing says a “very strong” economy like cutting rates by 100 basis points and launching quantitative easing.

The question to ask is: How will Trump react if they Fed doesn’t cut rates that aggressively and the US dollar continues to strengthen?

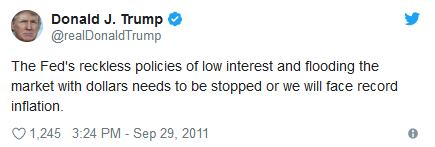

Back in 2011 when unemployment was at 9%.