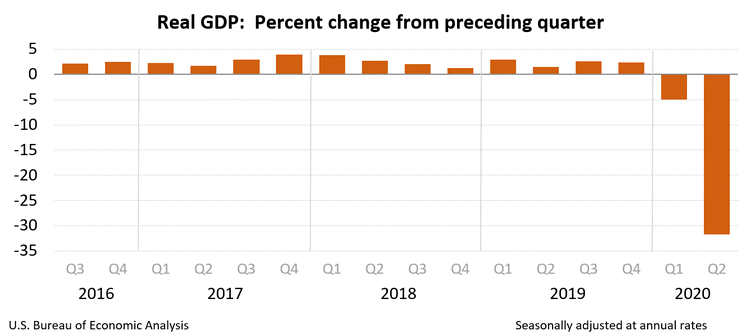

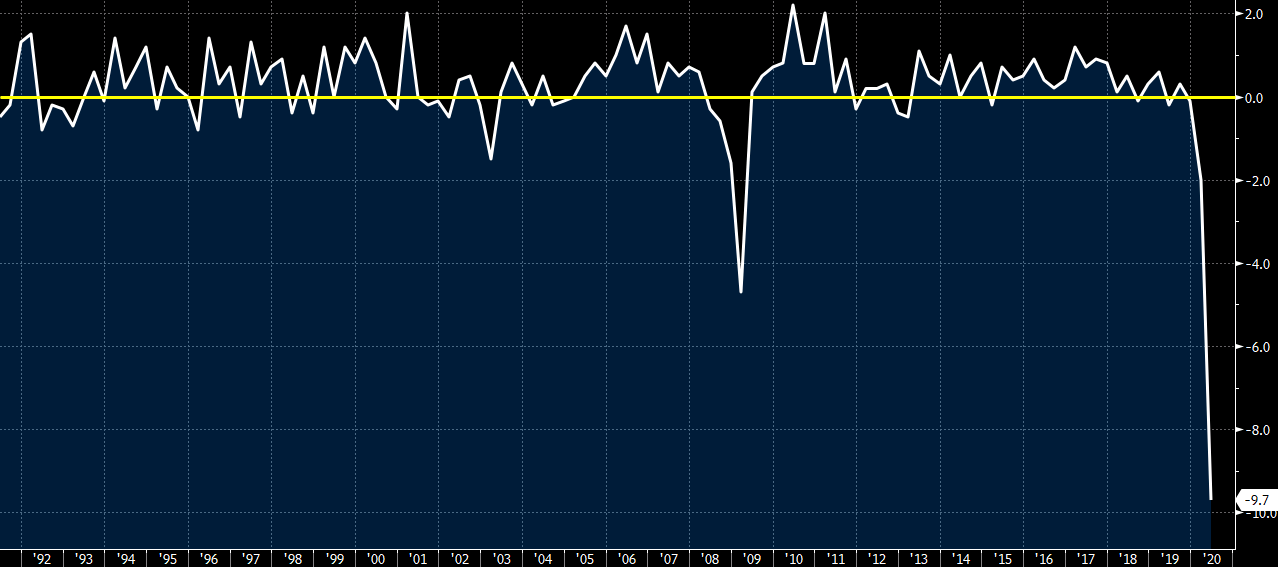

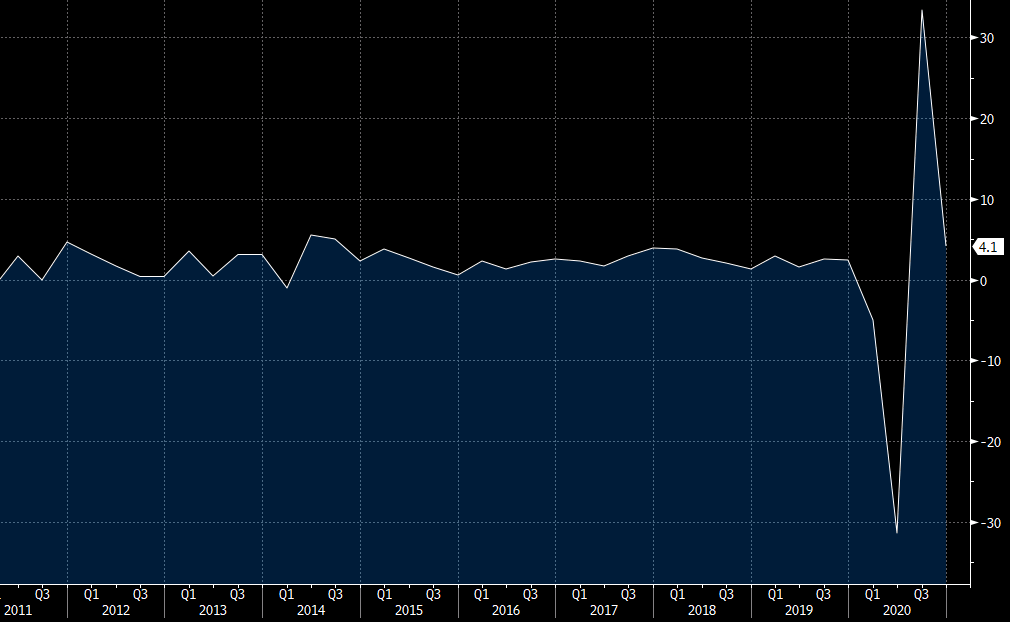

Fourth quarter 2020 GDP estimate

- First reading was +4.0%

- Final Q3 reading was +33.4%

- Personal consumption +2.4% vs +2.5% expected

- GDP price index +2.1% vs +2.0% expected

- Core PCE +1.4% vs +1.4% expected

- Deflator +2.0%

- Full report

Details:

- Ex motor vehicles +4.7% vs +4.5% prelim

- Final sales +3.0% vs +3.0% prelim

- Inventories added 1.11 pp to GDP vs 1.04 in prelim report

- Business investment +14.0% vs +13.8% prelim

- Business investment in equipment +25.7% vs +24.9% prelim

- Exports +21.8% vs +22.0% prelim

- Imports +29.6% vs +29.5% prelim

- Home investment +35.8% vs +33.5% prelim

The consumer was a tad weaker in Q4 than initial reports while business and home investment was a bit stronger. Overall, I don’t see anything here that will bleed into Q1 2021.