Massive week for European stock markets

Closing changes for the main bourses:

- German DAX +3.4%

- UK FTSE 100 +2.2%

- Italy MIB +2.7%

- French CAC +3.5%

- Spain IBEX +4.2%

On the week:

- German DAX +9.1%

- UK FTSE 100 +6.6%

- Italy MIB +10.9%

- French CAC +10.4%

- Spain IBEX +10.9%

When tack on a 2% rally in EUR/USD the gains look even better. With gains like this you can see why money is flowing into the euro.

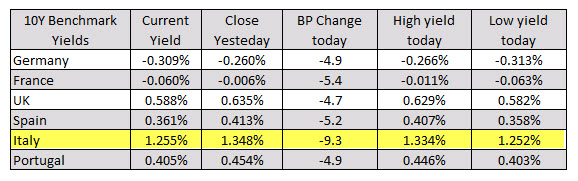

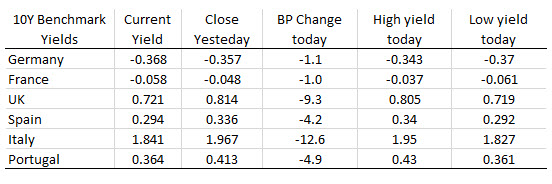

The run in Italian stocks has been spectacular: