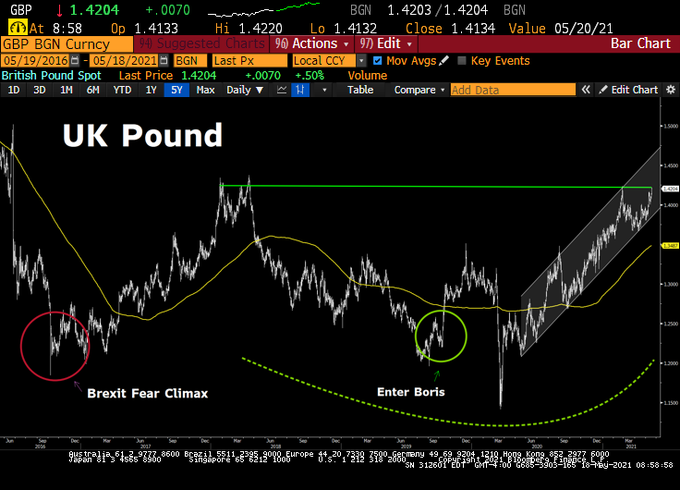

The BOE and UK local elections are the two event risks to watch

The BOE could make an announcement to taper QE purchases later in the day, though there is some expectation that they may put that off until June or perhaps even August. That said, they could still tee that up with a more hawkish tone this time around.

Meanwhile, the area to watch in the UK local elections is in Scotland and whether Nicola Sturgeon’s SNP will be able to garner a majority to potentially push forward with the agenda of a second Scottish independence referendum.

The main risk for the pound is if the BOE turns out more dovish than expected and fails to tick the boxes in terms of setting up expectations of a taper to follow and the SNP winning a majority in the local elections.

That said, I would expect dips to be bought with worries on the Scottish independence referendum likely to be phased out over time while the market continues to keep a firm focus on the more structural undertones in the pound.

The BOE may put off any taper or tightening talk this month but will inevitably have to address that by August at the latest as the economy reopens in a more meaningful way.