The estimate is unchanged from its January gauge of economic activity

The central bank also confirms that it sees French GDP growing by 5% for the year.

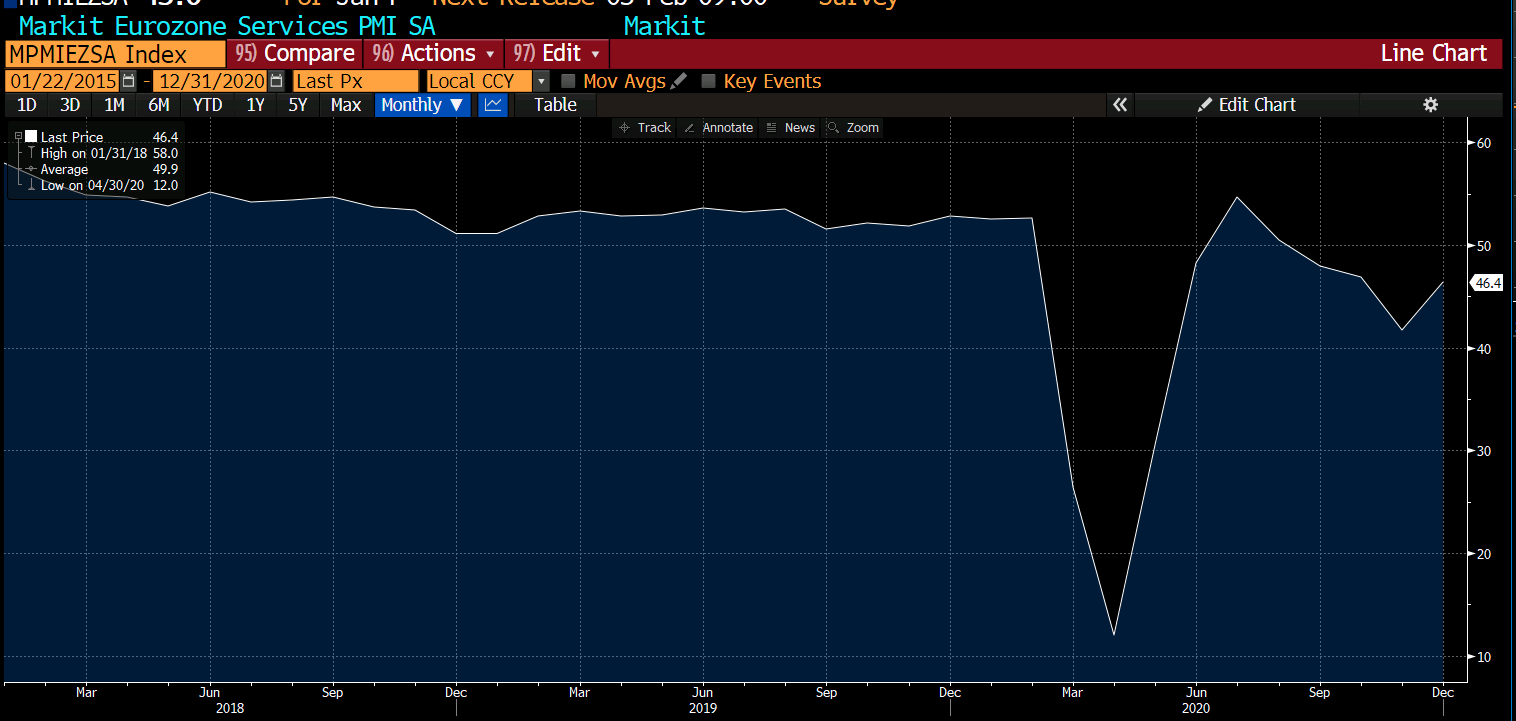

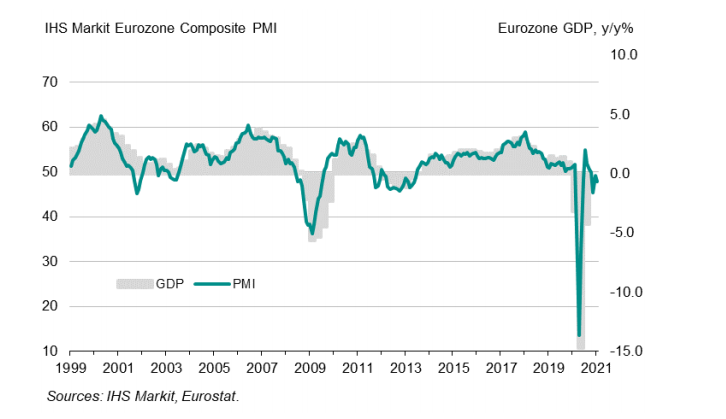

“The eurozone economy endured a predictably tough start to 2021 as ongoing efforts to contain the spread of COVID-19 continued to hit business activity, especially in the service sector. Manufacturing growth continued to help offset some of the weakness in the service sector, though even here factories saw output growth slow amid subdued demand and supply delays, often linked to the pandemic.

“A contraction of GDP therefore looks likely in the first quarter, though on current trends this should be modest in comparison to the falls seen in the first half of 2020.

“However, with virus containment measures likely to constrain euro area economies in the coming months, and potentially well into the second quarter given the slow vaccine roll-out, the focus will be on the need to sustain supportive fiscal and monetary policymaking for some time to come, notably to prevent further intensifying job losses in the hardest hit sectors, such as hospitality, tourism, travel and retail.

“Rising costs have dealt a further blow to many companies, with input prices rising at the steepest rate for two years to squeeze margins. However, in many cases this reflects a short-term lack of capacity and shipping delays, which should ease in coming months, helping alleviate these price pressures.”

Manufacturing 51.3

Non-manufacturing 52.4

Composite 52.8

—

Headlines via Reuters: