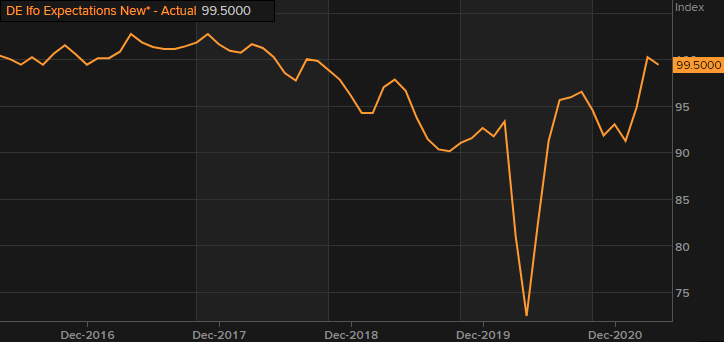

Latest data released by Ifo – 26 April 2021

- Prior 96.6

- Expectations 99.5 vs 101.2 expected

- Prior 100.4; revised to 100.3

- Current assessment 94.1 vs 94.4 expected

- Prior 93.0; revised to 93.1

Slight delay in the release by the source. The readings miss on estimates but the headline and current assessment show some mild improvement relative to March. That said, expectations see a drop and that may be tied to prolonged tighter restrictions.

As much as vaccine optimism is still part of the bigger picture, the prevailing virus situation does little to ease comfort as measures to curb the virus spread looks set to continue through to the latter stages of Q2 at the very least.