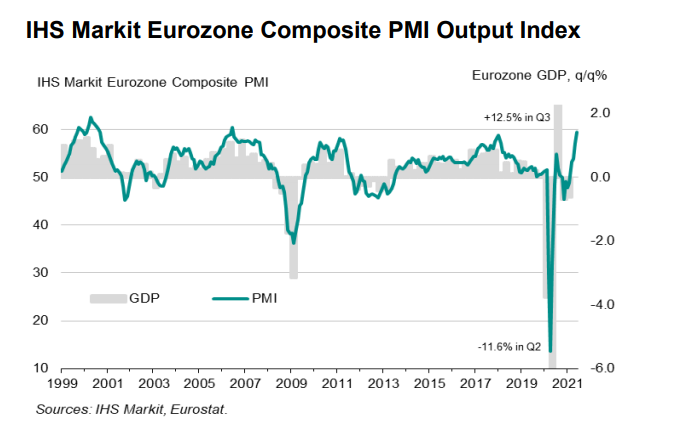

Latest data released by Markit – 5 July 2021

- Composite PMI 59.5 vs 59.2 prelim

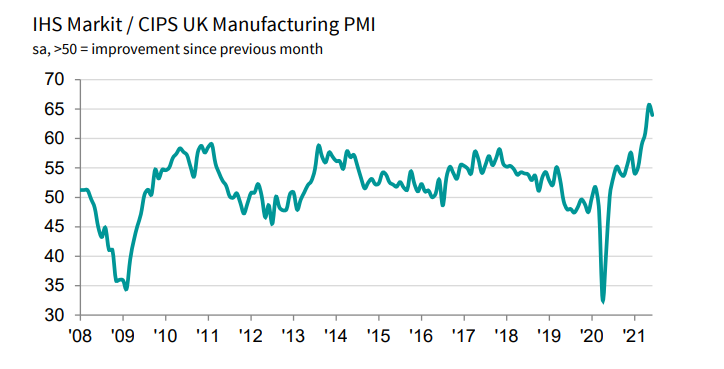

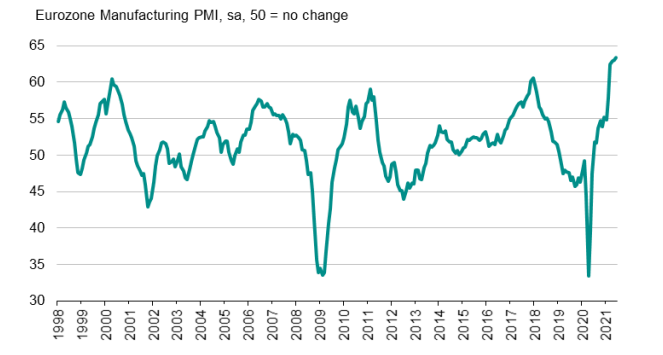

A slight revision higher on the balance of things and that marks the quickest growth in Eurozone activity in 15 years, with both the manufacturing and services sectors showing marked improvement as virus restrictions are loosened.

That said, supply disruptions are leading to higher cost inflation and that remains a threat to the recovery momentum if it continues persistently in the months ahead.

“Europe’s economic recovery stepped up a gear in June, but inflationary pressures have also ratcheted higher.

“Business is booming in the eurozone’s service sector, with output growing at a rate unsurpassed over the past 15 years. Added to the impressive growth seen in the manufacturing sector, the PMI surveys suggest the region’s economy is firing on all cylinders as it heads into the summer.

“Service sector growth has picked up across the board among the countries surveyed, with hard-hit sectors such as hospitality and tourism now coming back to life to join the recovery as economies and travel are opened up from virus-related restrictions.

“A wave of optimism that the worst of the pandemic is behind us has meanwhile propelled firms’ expectations of growth to the highest for 21 years, boding well for the upturn to gain further strength in coming months.

“Firms are increasingly struggling to meet surging demand, however, in part due to labour supply shortages, meaning greater pricing power and underscoring how the recent rise in inflationary pressures is by no means confined to the manufacturing sector. Service sector companies are hiking their prices at the steepest pace for over 20 years as costs spike higher, accompanying a similar jump in manufacturing prices to signal a broad-based increase in inflationary pressures.”