The German economy ministry brushes aside concerns from the impact of supply chain disruptions globally

- Outlook for the industrial sector as a whole remains positive

- Supply bottlenecks for intermediate products have dampening effect

- But it does not affect positive dynamics of overall economy

- German economic recovery seen to be at full swing at the end of Q2

This fits with the argument that most policymakers and lawmakers are stating for now, in that all of this is going to be ‘transitory’ and will work itself out once demand conditions pick up globally as the virus situation recedes.

That said, the environment remains challenging for emerging markets and that in itself cannot be underestimated as there is a ripple effect to the rest of the globe.

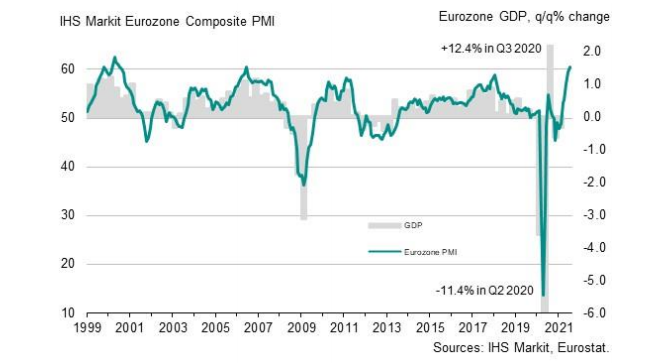

Anyway, speaking of supply issues, euro area industrial production for May is estimated to surprise downward because of that. Economist, Christophe Barraud, highlights the case for that in his post

here leading up to the report later.