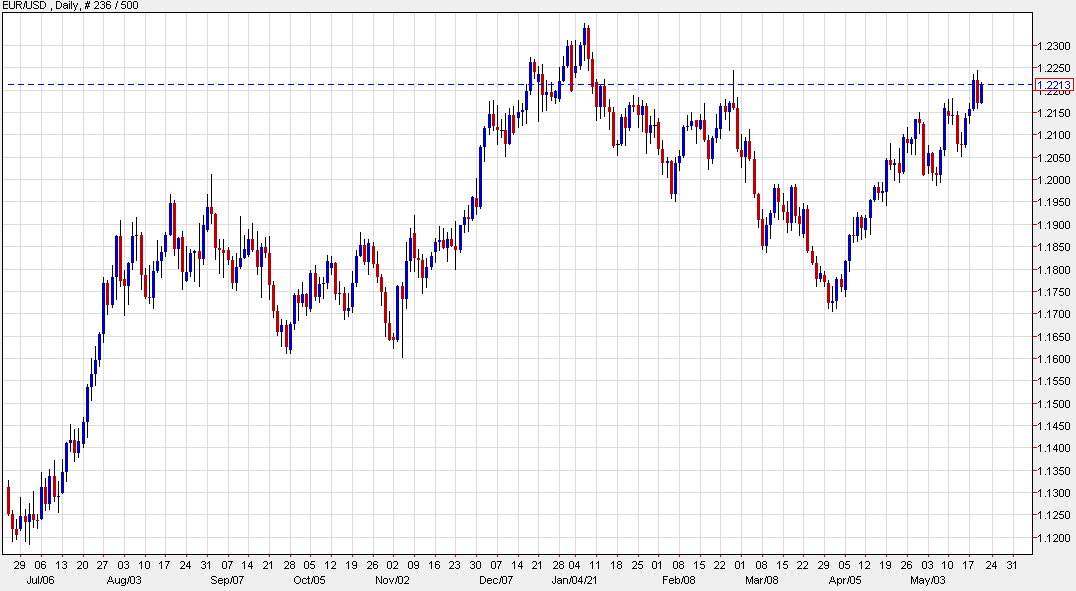

Major indices closing higher on the day. German DAX up 1.5%

The major European indices are rebounding from yesterday’s sharp declines which is all the German DAX fall -1.77%. Today that index is up 1.5% – nearly fully retracing the declines.

A look at the provisional closes are showing:

- German DAX, +1.5%

- France’s CAC, +1.2% (it fell -1.43% yesterday)

- UK’s FTSE 100, +0.9% (down -1.19% yesterday)

- Spain’s Ibex, +0.2%

- Italy’s FTSE MIB, +0.6%

In other markets as European/London traders look to exit,

- Spot gold is trading up $8.29 or 0.44% at $1877.90.

- Spot silver is up at $0.12 or 0.44% at $27.85

- WTI crude oil futures are trading down $0.39 or -0.62% at $62.97

- Bitcoin is rebounding by $3300 or 8.6% at $41,640

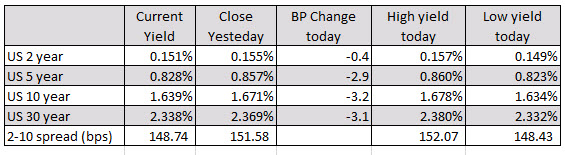

In the US debt market, yields are lower, led by a -3.2 basis point decline in the 10 year.

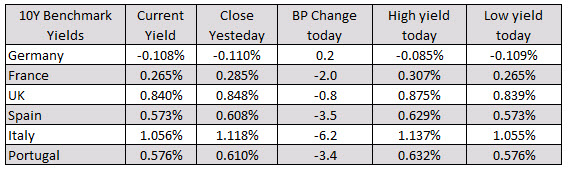

In the European debt market benchmark 10 year yields were also lower with the exception of a small 0.2 basis point gain in Germany.

In the European debt market benchmark 10 year yields were also lower with the exception of a small 0.2 basis point gain in Germany.

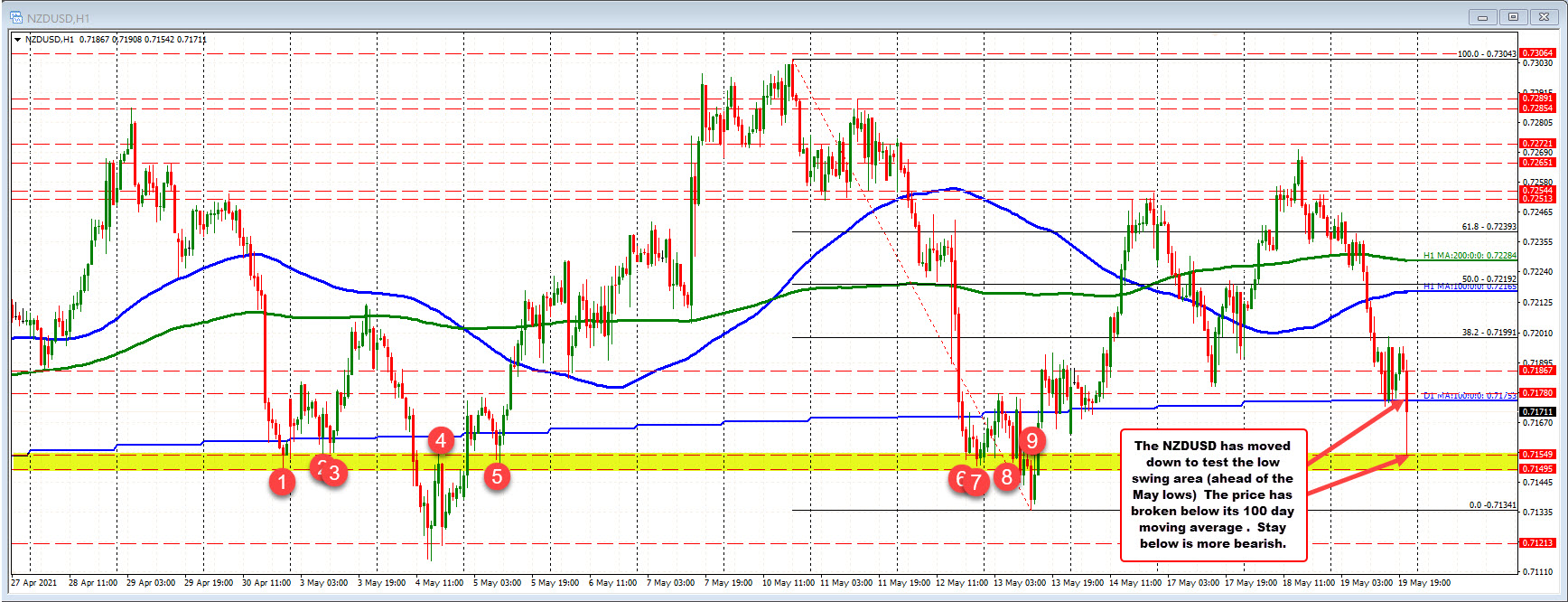

In the US stock market, the NASDAQ index is up 218 points or 1.64%, and in the process, has moved back above its 100 hour moving average at 13491. That tilts the bias more to the upside once again.