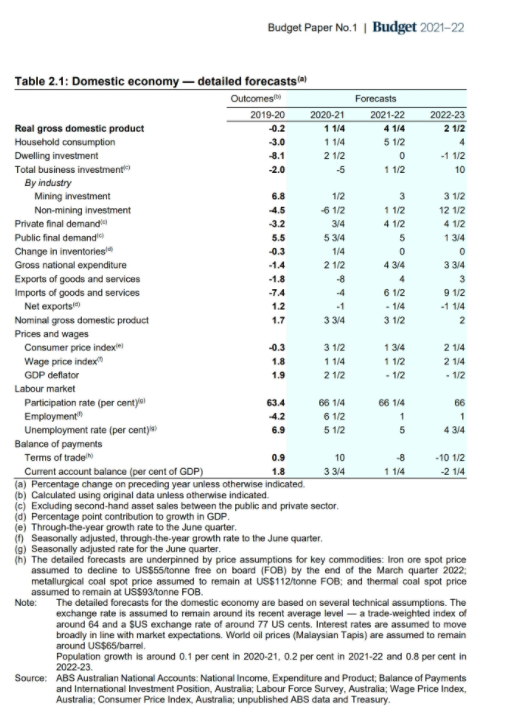

Schrödinger’s dumpster:

It has been tough to keep bond sellers at bay since the turnaround after the non-farm payrolls miss on Friday. 10-year yields fell to around 1.48% at the time but is now trading up to 13 bps higher at around 1.61% in European morning trade.

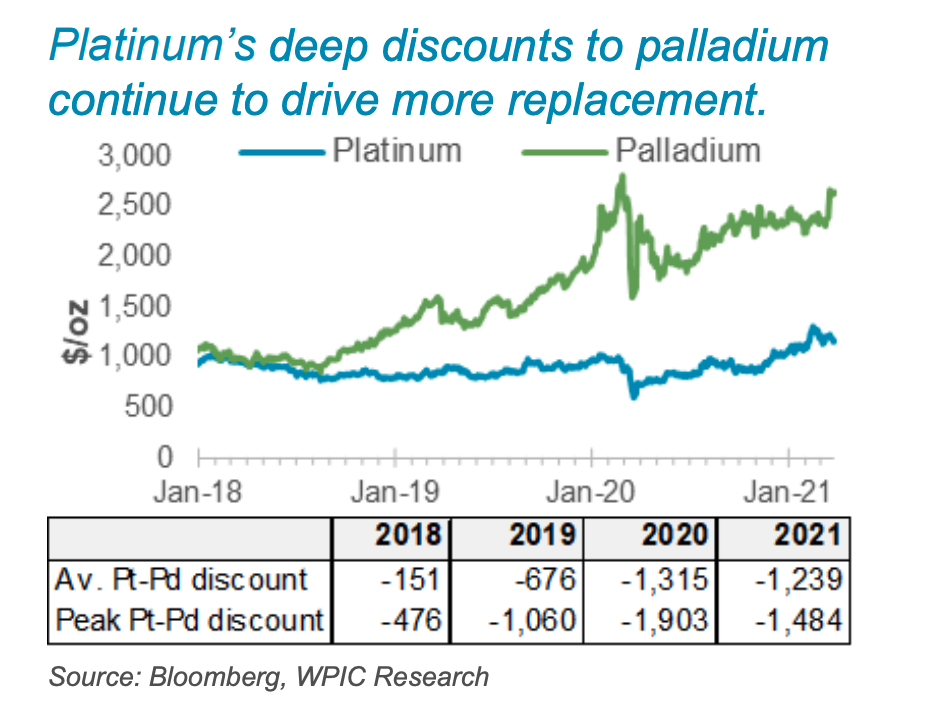

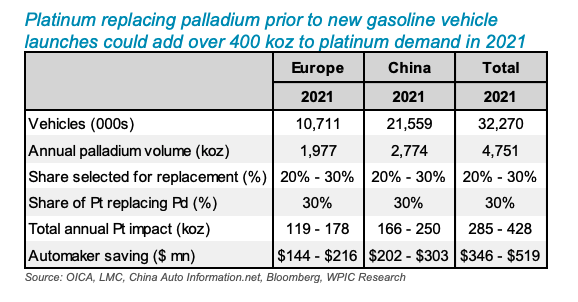

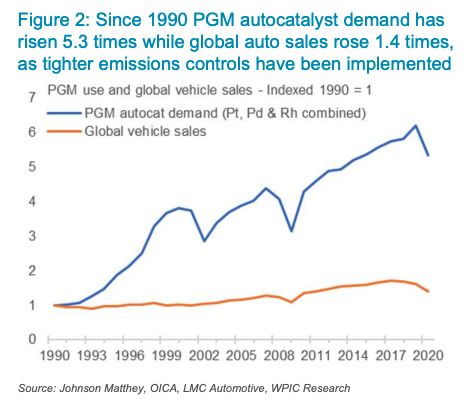

This is one area to watch/investigate further that I cam across this week and wanted to bring to readers attention. Some of the research I read is quite hard to actually extract the significant information from, so here is a potted summary of the main points:

See here and here for some more detail on the above points from the World Platinum Investment Council. The caveat is that the group’s purpose is to stimulate Platinum investment, but facts are facts so don’t dismiss the research out of hand.